Entrepreneur reviewing business structure options for one LLC versus multiple LLCs

How to Have Multiple Businesses Under One LLC?

Running more than one business is common among serial entrepreneurs and small business owners looking to diversify income streams. The question of whether to house all your ventures under a single LLC or create separate entities for each affects your taxes, liability exposure, and administrative workload for years to come.

Many business owners assume they need a new LLC every time they launch a venture. That's not always true. Understanding the legal structure options available—and their trade-offs—helps you make smarter decisions about protecting assets while keeping costs manageable.

Can You Legally Run Multiple Businesses Under One LLC?

Yes, you can legally operate multiple businesses under one LLC in all 50 states. No federal or state law prohibits a single limited liability company from engaging in different business activities or serving multiple markets.

Your LLC's operating agreement and articles of organization typically don't restrict the number of ventures you can run. Most states allow you to list a broad business purpose when forming your LLC—something like "any lawful business activity"—which gives you flexibility to expand into new areas without amending your formation documents.

However, there's a common misconception that you automatically get separate liability protection for each business just because they operate under one LLC umbrella. That's incorrect. A single LLC creates one legal entity, which means all businesses share the same liability shield. If someone sues one of your ventures, they can potentially reach the assets of all businesses within that LLC.

State requirements vary mainly in how you register additional business names. Some states require DBA (Doing Business As) filings at the county level, while others handle them through the Secretary of State's office. Registration fees range from $10 to $100 depending on your location.

Author: Kevin Halbrook;

Source: worldwidemediums.net

One practical consideration: certain licensed professions face restrictions. For example, many states prohibit combining a law practice with unrelated businesses in the same LLC. Check your industry's licensing board requirements before consolidating ventures.

Two Ways to Structure Multiple Businesses in One LLC

When you want to operate separate businesses under one legal entity, you have two primary structural approaches. Each serves different needs and comes with distinct administrative requirements.

Using DBAs (Doing Business As) for Different Business Names

A DBA lets your LLC operate under a different public-facing name without creating a new legal entity. Your LLC remains the legal owner, but customers see the DBA name on storefronts, websites, and marketing materials.

Here's how it works: If your LLC is named "Riverside Ventures LLC," you might register DBAs like "Riverside Catering" and "Riverside Event Planning." Legally, Riverside Ventures LLC owns both businesses, but each has its own brand identity.

The registration process is straightforward. You file a DBA certificate with your county clerk or state business office, depending on your state's rules. Most jurisdictions require renewal every three to five years. After registration, you can open bank accounts in the DBA name (though the LLC remains the account owner) and use the name in contracts.

DBAs work best when your businesses are related or target similar customer bases. A landscaping company adding a snow removal service makes sense under one LLC with two DBAs. The businesses share similar liability profiles, equipment, and seasonal workflows.

The main limitation: DBAs don't create legal separation. All businesses under your LLC share the same tax ID number, bank accounts (unless you specifically open separate ones), and liability exposure.

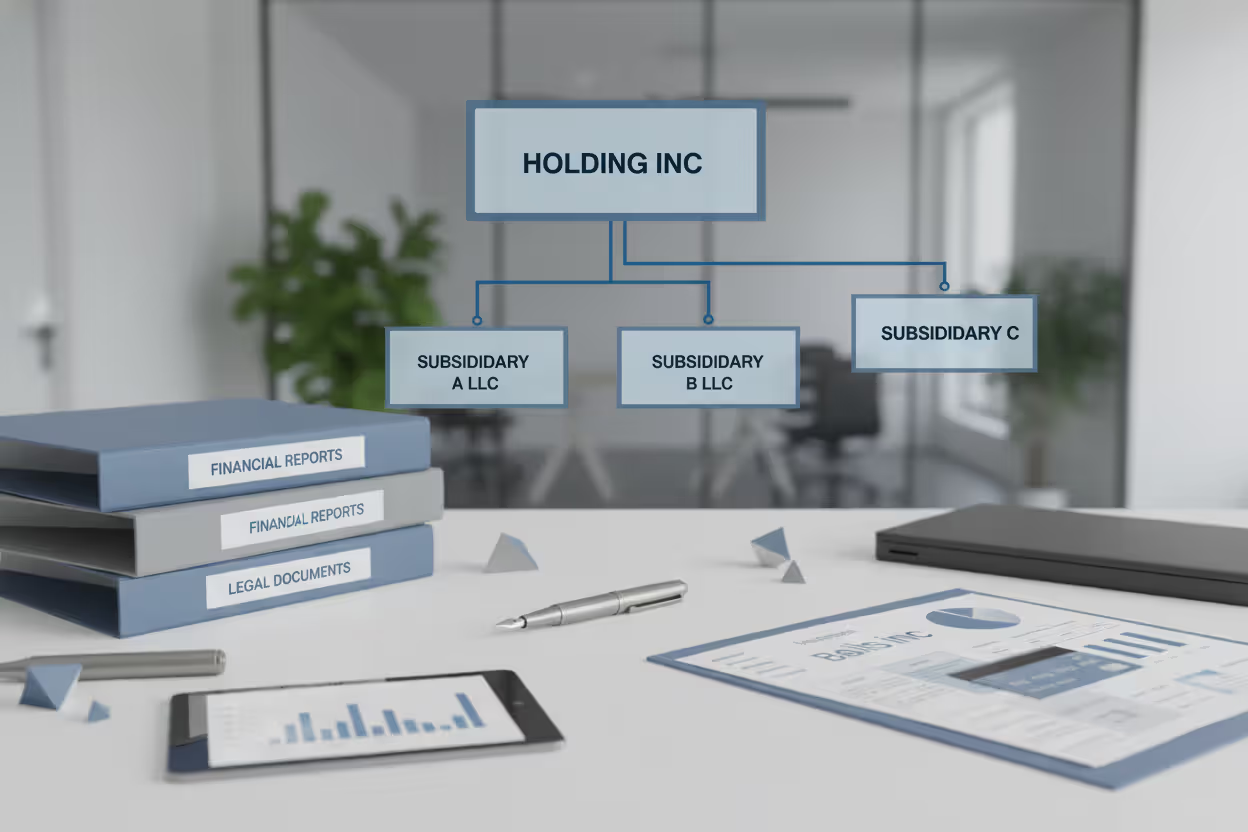

Creating Separate LLCs with a Holding Company

A holding company structure involves creating multiple LLCs—one for each business—with a parent LLC that owns them all. This approach provides true legal separation between ventures while maintaining centralized ownership.

For example, you might form "Summit Holdings LLC" as your parent company, which then owns 100% of "Summit Retail LLC" and "Summit Consulting LLC." Each subsidiary operates independently with its own bank accounts, tax filings, and liability protection.

Author: Kevin Halbrook;

Source: worldwidemediums.net

This structure costs more upfront. You'll pay formation fees for each LLC (typically $50–$500 per state) plus annual fees and registered agent costs. Some states charge franchise taxes based on revenue, multiplying your annual expenses.

The payoff comes in liability protection. If Summit Retail LLC faces a lawsuit, the plaintiff generally can't reach assets held by Summit Consulting LLC or Summit Holdings LLC (assuming you maintain proper corporate formalities and don't commingle funds).

Holding companies make sense when you're running high-risk businesses, planning to bring in investors for specific ventures, or building businesses you might sell individually. Real estate investors commonly use this structure, creating separate LLCs for each property with a holding company on top.

Advantages of Putting Multiple Businesses Under One LLC

Cost savings represent the most immediate benefit. You'll pay one set of formation fees, one registered agent fee, and one annual state filing fee instead of multiplying these costs across several entities. For business owners in California, where LLCs pay an $800 annual franchise tax, running three businesses under one LLC saves $1,600 per year compared to three separate LLCs.

Tax filing becomes simpler with one entity. Your LLC files a single tax return (or passes through to your personal return if you're a single-member LLC). You don't need to track separate books for each venture or pay your accountant to prepare multiple returns. This consolidation typically saves $500–$2,000 annually in accounting fees.

Administrative efficiency improves when you're not juggling multiple entities. You maintain one operating agreement, one set of corporate records, and one compliance calendar. Renewals, amendments, and state filings happen once instead of several times.

Cash flow management becomes easier when all businesses share one bank account. You can shift money between ventures without formal loans or documentation. If your consulting business has a slow month but your e-commerce store performs well, the profits naturally offset each other.

Startup businesses particularly benefit from this structure. When you're testing new ideas or pivoting frequently, creating a new LLC for every experiment creates unnecessary paperwork and expense. One LLC with multiple DBAs lets you launch and shut down ventures quickly.

Risks and Drawbacks of One LLC for Multiple Businesses

Liability exposure represents the biggest concern. When all your businesses operate under one LLC, a lawsuit against any single venture puts all your assets at risk. If your food truck causes food poisoning, the plaintiff can potentially reach profits from your unrelated graphic design business that operates under the same LLC.

Author: Kevin Halbrook;

Source: worldwidemediums.net

This risk multiplies when you combine high-liability businesses with low-risk ones. Imagine running a tree removal service (high risk of property damage or injury) alongside a low-risk online course business. One accident with the tree service could expose the course business revenue and assets.

Commingled assets create problems during audits, lawsuits, or sales. When multiple businesses share bank accounts and financial records, distinguishing which expenses belong to which venture becomes difficult. This confusion can trigger IRS scrutiny and makes it nearly impossible to calculate accurate profit margins for individual businesses.

Selling one business while keeping others becomes complicated. Buyers typically want to purchase a standalone entity with clean financials and clear asset ownership. When your businesses are intertwined in one LLC, you'll need to spin off the business into a new entity before selling—adding time, legal fees, and complexity to the transaction.

Tax complications can arise if your businesses have different structures or state tax obligations. Operating businesses in multiple states under one LLC means your entire entity might owe taxes in each state, not just the business operating there. Some states impose franchise taxes based on total company revenue, increasing your tax burden.

Insurance costs may increase. Some insurers charge higher premiums when one policy must cover multiple business activities, especially if those activities carry different risk profiles. You might pay more for a single policy covering both your consulting practice and your equipment rental business than you would for two separate policies.

Investor and lender requirements often specify separate entities. If you want to raise capital for one business, investors typically prefer a clean corporate structure where they own shares in a standalone company, not a percentage of an LLC running multiple ventures.

When You Should Use Separate LLCs Instead

High-risk industries demand separate entities. If you own rental properties, a construction company, or any business with significant liability exposure, isolate each venture in its own LLC. Real estate investors commonly create one LLC per property. The extra annual fees pale in comparison to the asset protection you gain.

Unrelated business types benefit from separation. Running a medical practice and a restaurant under one LLC creates unnecessary complications. These businesses have different licensing requirements, insurance needs, customer bases, and risk profiles. Separate LLCs simplify management and protect each venture from the other's liabilities.

Growth plans requiring outside investment need standalone entities. Venture capitalists and angel investors won't invest in one business buried inside an LLC that operates three others. They want clear ownership stakes, clean financials, and the ability to exit their investment by selling their shares in a specific company.

Partnership situations where different people own different businesses require separate LLCs. If you own 100% of an e-commerce store but partner 50/50 with someone on a software business, these ventures need distinct entities with their own operating agreements and ownership structures.

Franchise agreements typically require separate entities. Most franchisors mandate that each franchise location operates through its own LLC to maintain clear liability boundaries and simplify their legal relationships with franchisees.

Geographic expansion into multiple states often justifies separate LLCs. While you can register one LLC as a foreign entity in multiple states, this approach means your entire company owes taxes and fees in each state. Creating state-specific LLCs can reduce your overall tax burden and simplify compliance.

Author: Kevin Halbrook;

Source: worldwidemediums.net

Steps to Add a New Business to Your Existing LLC

Review your operating agreement first. Check whether your current agreement limits business activities or requires member approval to expand into new ventures. Most standard operating agreements won't restrict you, but custom agreements might include specific limitations.

Comparison: One LLC with DBAs vs. Separate LLCs

| Feature | One LLC with DBAs | Separate LLCs |

| Formation cost | $50–$500 (one-time) | $50–$500 per LLC |

| Annual fees | $50–$800 (single fee) | $50–$800 per LLC |

| Liability protection | Shared across all businesses | Isolated per LLC |

| Tax filing | One return | Multiple returns |

| Administrative complexity | Low | High |

| Selling a business | Difficult; requires restructuring | Simple; sell the LLC |

| Best for | Related, low-risk businesses | Unrelated or high-risk ventures |

Amend your operating agreement if necessary. Add language describing the new business activity and how profits will be allocated among members. This documentation protects all owners by clarifying expectations before launching the new venture.

Register a DBA if you want a different business name. Visit your county clerk's office or state business filing office (depending on your state) and file a fictitious name certificate. Bring your LLC's articles of organization and a government-issued ID. The process usually takes 10–20 minutes, and fees range from $10–$100.

Update your business licenses and permits. Your new business activity might require additional licenses your current LLC doesn't hold. A restaurant adding catering services needs different health department permits. An online retailer opening a physical store needs local business licenses.

Check your EIN situation. Most businesses won't need a new EIN when adding ventures to an existing LLC. Your current EIN covers all business activities under that legal entity. The exception: if your LLC's tax classification changes (for example, electing S-corporation status), you'll need a new EIN.

Open separate bank accounts for each business, even though they're under one LLC. This separation simplifies bookkeeping and creates clear financial records for each venture. Tell your bank you're opening an account under your LLC's DBA name.

Notify your insurance carrier. Your current business insurance policy might not cover new business activities. If your LLC operates a consulting business and you add product sales, your general liability policy needs updating to cover product liability claims.

Update contracts with vendors, suppliers, and service providers. Clarify which business within your LLC is entering agreements. Instead of signing as "Smith Ventures LLC," specify "Smith Ventures LLC d/b/a Smith Consulting" on relevant contracts.

Revise your bookkeeping systems to track income and expenses separately for each business. Use accounting software categories, classes, or separate company files to maintain distinct financial records. This separation becomes critical during tax preparation and if you later decide to sell one business.

The biggest mistake I see entrepreneurs make is mixing high-risk and low-risk businesses in one LLC to save on filing fees.They'll run a profitable online business and a rental property under the same entity. When a tenant sues over a slip-and-fall, suddenly their entire online business revenue is exposed. The $800 they saved on annual fees can cost them hundreds of thousands in a lawsuit

— Jennifer Martinez

FAQ: Multiple Businesses Under One LLC

Deciding whether to operate multiple businesses under one LLC comes down to balancing cost savings against risk management. The single-entity approach works well when you're running related, low-risk ventures and want to minimize administrative overhead and expenses.

Create separate LLCs when your businesses carry significant liability, serve completely different markets, or when you plan to bring in investors or eventually sell individual ventures. The extra cost buys you genuine asset protection and operational flexibility.

Most business owners benefit from starting with one LLC and using DBAs for additional ventures. As your businesses grow and generate substantial revenue, transition high-risk or high-value ventures into separate entities. This phased approach lets you test ideas affordably while scaling your asset protection as your exposure increases.

Whichever structure you choose, maintain clean financial records for each business, even if they're under one LLC. Separate bank accounts, detailed bookkeeping, and clear documentation protect you during audits, lawsuits, and eventual business sales. Consult with a business attorney and CPA familiar with your state's laws before making structural decisions that affect your liability and tax obligations for years to come.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Limited Liability Companies (LLCs), including formation, management, taxation, compliance, and business structuring.

All information on this website, including articles, guides, templates, and examples, is presented for general educational purposes. LLC requirements and regulations may vary depending on individual circumstances, business activities, state laws, and jurisdiction.

This website does not provide legal, tax, or financial advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.