Business owner reviewing documents for S corporation to LLC conversion in an office

How to Convert an S Corp to LLC?

Restructuring your S corporation into an LLC takes months, not days. You're rebuilding your business's legal foundation while keeping operations running—touching everything from IRS registrations to vendor contracts.

Most owners pursue this change when corporate formalities become burdensome, when they need ownership structures that S corps can't accommodate, or when their original entity choice no longer matches how they actually run things.

The work ahead involves multiple government agencies, several thousand dollars in costs, and permanent changes to your tax situation. I've seen businesses save $8,000 yearly after converting. I've also watched others get hit with $15,000 in unexpected self-employment taxes they didn't anticipate. This guide walks through the actual mechanics of conversion so you can make an informed choice for your specific circumstances.

Why Business Owners Convert from S Corp to LLC

Most conversions I see stem from one persistent frustration that won't resolve any other way.

Corporate Formalities Become Overhead

S corps require board meetings, written minutes documenting decisions, and formal resolutions—even when you're the only shareholder making obvious business calls. Skip these formalities during a busy quarter and you've created audit exposure that could terminate your S election. LLCs operate differently. Make decisions without documentation trails. No mandatory meetings. No required minutes for routine choices. A two-person consulting firm I worked with calculated they spent 18 hours annually on corporate formalities that added zero value to their operations. They converted last year.

Ownership Rules Create Real Problems

Your S corp maxes out at 100 shareholders. No corporate shareholders. No partnerships as owners. No nonresident aliens. Most trusts don't qualify either. These restrictions sound theoretical until you actually need a foreign investor or want to set up a qualified ESOP trust. I reviewed one medical practice that needed to bring in a Canadian specialist as part-owner. Their S corp structure made that impossible without conversion. After restructuring as an LLC, they closed the deal within six weeks. LLCs accept unlimited members of any type—individuals, businesses, foreign investors, trusts, whatever your situation requires.

Author: Daniel Whitlock;

Source: worldwidemediums.net

Profit Allocation Follows Stock Ownership

S corporations lock you into pro-rata distributions matching ownership percentages exactly. Someone owns 30% of shares? They receive 30% of distributions, no exceptions. LLCs let your operating agreement override this default. You might give your operations partner 60% of distributions despite only 40% equity ownership because they're doing most of the work. Or shift tax losses toward the member who needs deductions most. A software company I advised splits profits 50-30-20 among three members who each own one-third equity. Their operating agreement bases distributions on contribution levels rather than equal ownership. S corps can't do this.

Trading Payroll Complexity for Self-Employment Tax

S corp owners pay FICA taxes only on salary, avoiding those taxes on additional distributions. Someone taking $50,000 salary plus $90,000 distributions saves approximately $11,250 compared to paying 15.3% self-employment tax on the full $140,000. That savings comes with mandatory payroll processing, quarterly filings, and exposure to IRS challenges about "reasonable compensation." LLC members usually owe self-employment tax on their complete profit share—15.3% on amounts up to $168,600 in 2024, then 2.9% Medicare tax on everything above. Some owners accept paying more tax to eliminate payroll administration and audit risk. Others maintain S corp tax status while using LLC legal structure.

State Fee Structures Differ Wildly

Entity type affects state fees dramatically in some jurisdictions. California charges S corps an $800 franchise tax plus gross receipts fees reaching $11,790 for high-revenue businesses. The same business structured as a California LLC pays exactly $800 annually regardless of revenue. That's potentially $10,990 saved every year from entity structure alone. Meanwhile Delaware charges LLCs higher fees than corporations. Your state's specific fee schedule matters more than general advice.

Exit Strategies Work More Smoothly

Planning to close your business or sell to an acquirer? LLC dissolution generally requires fewer procedural steps. Corporate shutdowns demand final shareholder meetings, multiple board resolutions, and extensive documentation. LLC operating agreements typically establish simpler procedures for winding down operations and distributing remaining assets among members.

Legal Requirements for S Corp to LLC Conversion

Changing from corporation to llc means satisfying state business entity laws and federal tax regulations that operate independently.

State Filing Requirements

Your Secretary of State controls the entity transformation process. Required filings depend entirely on where your business is registered.

Direct Conversion in Most States

Forty-seven states now permit statutory conversion without dissolving anything. Your business maintains legal continuity—identical formation date, unchanged contracts, preserved licenses, just different entity classification. You'll usually need to:

- Complete conversion articles prescribed by your state (each state calls these something different)

- Submit LLC formation paperwork simultaneously

- Pay filing fees ranging from $40 in Mississippi to $520 in Massachusetts

- Obtain shareholder approval through a vote (threshold varies—could be simple majority or two-thirds depending on state law and your bylaws)

- Settle any overdue corporate reports and outstanding state fees

Processing takes one to four weeks in most states assuming your paperwork's clean.

Two-Step Process in Holdout States

Three states still don't recognize statutory conversion. There you'll form a completely new LLC, transfer everything to that entity, then formally dissolve your corporation. It's messier because you'll:

- File LLC formation documents as a brand-new entity application

- Prepare assignment agreements for every significant asset category

- Retitle real estate, vehicles, and intellectual property individually

- Provide written notice to all creditors about the entity change

- Submit corporate dissolution paperwork separately

- Possibly publish dissolution notices in newspapers (state-specific requirement)

This approach costs significantly more and stretches to two or three months instead of three to four weeks.

Federal Tax Elections and IRS Notifications

Changing your state entity type doesn't automatically change your federal tax classification. That requires separate IRS filings.

Terminating S Corporation Tax Status

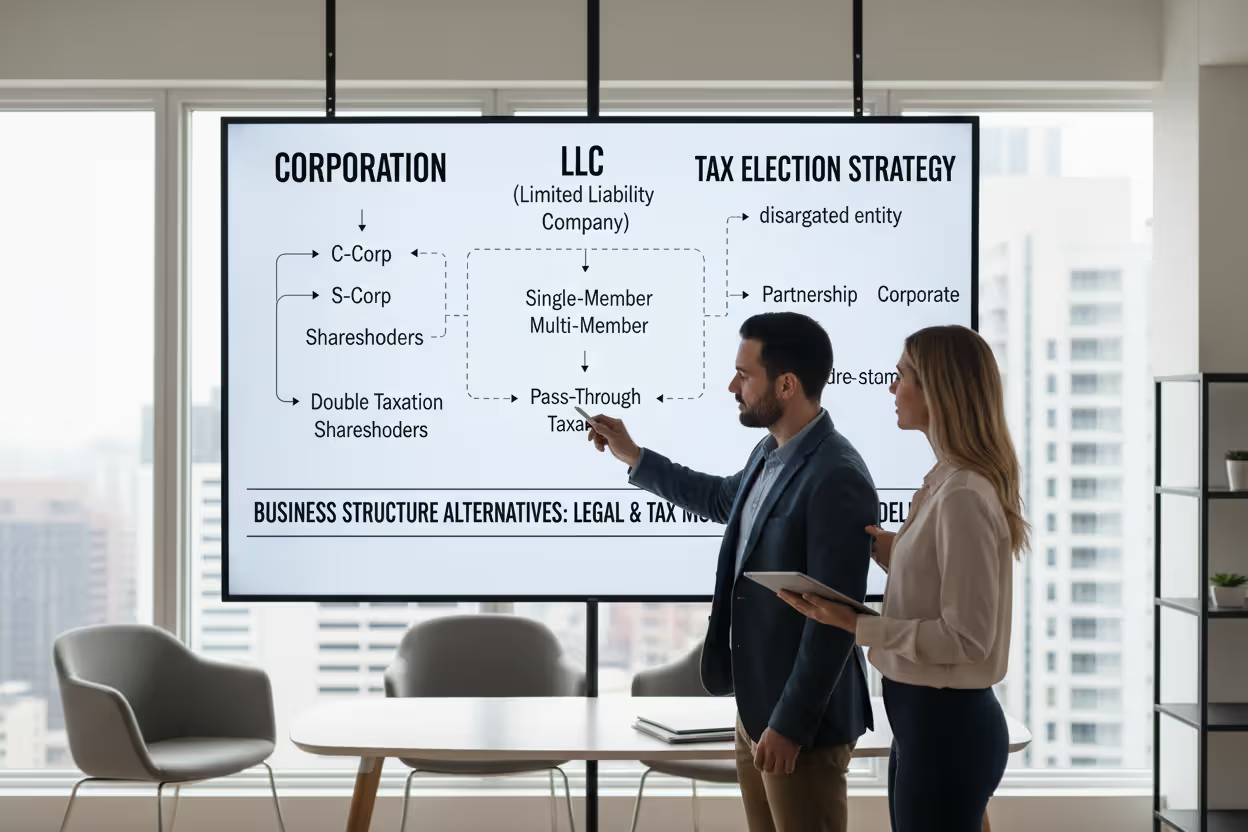

You'll file Form 1120-S one final time covering your last tax year. Write "FINAL RETURN" across the top so the IRS knows your S corp period ended. When your corporation dissolves, the S election automatically terminates. Statutory conversions work differently—your LLC initially inherits whatever tax classification the S corp had. You then choose whether to maintain that S election (by filing Form 2553 for the LLC within 75 days) or switch to default LLC taxation where the IRS treats single-member LLCs as sole proprietorships and multi-member LLCs as partnerships.

EIN Continuity Questions

Statutory conversion typically preserves your existing Employer Identification Number. You're not creating a separate entity, just modifying its legal form. Only dissolution-and-formation forces you to obtain a fresh EIN using Form SS-4, which then requires updating that number with banks, vendors, clients, state agencies, and every other organization that has your old EIN on file.

State Tax Account Updates

Every state tax registration you hold—sales tax permits, employer withholding accounts, corporate income tax registrations—needs amendment reflecting your new entity type. Most states impose 30-day deadlines for these notifications after conversion becomes effective. Miss those deadlines and you're looking at penalties or potentially having your registrations suspended.

Step-by-Step Process to Change S Corp to LLC

Converting s corp to llc works best when you follow a systematic sequence rather than jumping between tasks randomly.

Step 1: Secure Internal Approval

Draft a board resolution recommending conversion and explaining the business rationale. Present this to shareholders for formal vote, following whatever approval thresholds your bylaws and state law establish. Document everything through corporate minutes. Some states accept 51% approval, others demand two-thirds, and some require even higher thresholds. I watched one client nearly miss their conversion deadline because their bylaws required 80% approval but they'd initially planned for simple majority.

Step 2: Draft Your Operating Agreement

Never file state conversion documents until you've written a solid operating agreement first. This document replaces your corporate bylaws and governance structure. Address LLC management (member-managed versus manager-managed), capital contribution requirements, profit and loss allocation methods, member voting procedures, and provisions handling member withdrawal or business dissolution. Your former shareholders become LLC members, usually receiving ownership percentages matching their previous stock holdings unless you negotiate different arrangements.

Step 3: Submit State Filings

Send conversion paperwork and LLC formation documents to your state's business entity filing office. You'll specify the LLC name (verify availability first through name search), identify your registered agent, indicate whether members or appointed managers will run operations, and state your business purpose. Filing fees vary from roughly $90 in budget-friendly states like Kentucky to $500 or above in expensive jurisdictions like Massachusetts. Most states complete processing within two to three weeks, faster if you pay expedite fees.

Step 4: Update Every License and Permit

Pull out every business license, professional certification, health permit, and industry-specific authorization you've obtained. Each requires notification about your entity change. Some need formal amendments. Others demand complete reissuance. Professional licenses often process slowly—your state medical board or contractor licensing agency might take two months to approve a straightforward entity update. Start this immediately or you'll face periods where you legally cannot operate while waiting for updated approvals.

Step 5: Address Contracts and Agreements

Review every contract, lease, loan agreement, and vendor relationship carefully. Look for change-of-control provisions or anti-assignment clauses that might require counterparty consent before you convert. Even when consent isn't legally mandated, notify everyone you do business with about the entity change. It preserves relationships and prevents confusion when your LLC name appears instead of your corporate name on invoices. I know a contractor who lost a $200,000 client because they converted without notification and the client believed fraudulent invoices were being submitted.

Author: Daniel Whitlock;

Source: worldwidemediums.net

Step 6: Update Banking Relationships

Bring your conversion documents to your bank and update account ownership records. Some banks amend existing accounts in place. Others require closing corporate accounts and opening fresh LLC accounts, which is inconvenient but workable. Don't overlook merchant accounts for credit cards, payment processors like PayPal or Stripe, and any business credit cards or credit lines. Each requires separate notification and supporting documentation.

Step 7: Handle Tax Agency Notifications

Submit your final S corporation tax return with "FINAL RETURN" written prominently. Notify your state revenue department about the entity change. Update every tax registration—sales tax collector permits, payroll withholding accounts, income tax registrations. If you want your LLC taxed differently from default classification (disregarded entity for single-member LLCs, partnership for multi-member), submit Form 8832 to elect your preferred treatment. This election must be filed within 75 days of formation to take effect for your first tax year. Miss that window and you're locked into default taxation for at least twelve months.

Step 8: Amend Insurance Policies

Contact every insurance carrier you work with—general liability, professional liability, property coverage, workers' compensation. Amend policies so the LLC appears as the named insured. Skipping this step can void coverage entirely. Your insurance company might reject a claim if the policy names your defunct S corp but your LLC is the entity that actually experienced the loss.

Step 9: Complete Corporate Closeout

File any outstanding corporate reports your state requires, pay remaining franchise taxes, and formally dissolve the S corp if your state's conversion process demands it. Retain all corporate records for minimum seven years (some states mandate longer retention). You may need these documents for tax audits, litigation, or future business transactions.

Tax Implications When You Convert Corporation to LLC

The tax side of s corp to llc conversion gets technical quickly and varies based on your conversion method and subsequent tax elections.

S Corporation Election Termination

Converting to LLC structure ends your S corporation tax election. For direct conversions, this occurs automatically on the effective conversion date. The positive news is that the IRS generally treats properly executed conversions as tax-free reorganizations under Internal Revenue Code Section 368, meaning you won't trigger immediate taxes simply from converting.

Your LLC now needs tax classification. Single-owner LLCs automatically become disregarded entities—the IRS treats you like a sole proprietorship for tax purposes. Multi-owner LLCs default to partnership taxation. You can elect corporate taxation by submitting Form 8832, or even elect S corp tax treatment for your LLC by filing Form 2553 within 75 days. Many businesses convert to LLC legal structure while maintaining S corp taxation to preserve the salary-plus-distribution tax strategy.

Built-In Gains Tax Concerns

If your S corp previously operated as a C corporation, you might still be within the five-year built-in gains recognition period. Converting to LLC doesn't eliminate this potential tax liability. Any appreciated assets you sell during that recognition period still trigger built-in gains tax at the entity level, identical to what would have happened before conversion.

Basis Calculations and Documentation

The basis you held in S corp stock converts to basis in your LLC membership interest. For statutory conversions, this generally transfers without adjustment. When using the dissolution-and-formation method, you need detailed basis documentation. Calculate incorrectly and you'll report taxes wrong when you eventually sell your membership interest or receive distributions. The IRS won't accept "I think my basis was approximately $50,000" during an audit three years later.

Self-Employment Tax Changes Everything

This frequently represents the largest tax impact in s corp to llc conversion. S corp owner-employees pay FICA only on reasonable salary amounts. Additional distributions avoid the 15.3% self-employment tax. LLC members generally owe self-employment tax on their complete share of business income—15.3% on the first $168,600 for 2024, plus 2.9% Medicare tax on all amounts exceeding that threshold.

For profitable businesses, this change can cost $12,000-$35,000 annually in additional taxes. A business owner receiving $65,000 salary plus $85,000 distributions as an S corp pays FICA on just the $65,000. Convert to an LLC taxed as a partnership and suddenly they're paying self-employment tax on the full $150,000. That's an extra $13,005 in annual taxes. Some businesses avoid this by having the LLC elect S corporation taxation, preserving the salary-and-distributions approach while gaining LLC flexibility.

Author: Daniel Whitlock;

Source: worldwidemediums.net

State Tax Treatment Varies Dramatically

State tax treatment differs drastically across jurisdictions. Some states impose higher taxes on LLCs than S corps. Others do the reverse. California charges LLCs a gross receipts fee from $900 to $11,790 based on total income, on top of the standard $800 franchise tax. New York City assesses LLCs an unincorporated business tax that doesn't apply to corporations. Tennessee completely exempts S corps from state income tax but taxes LLCs. Research your specific state's approach before converting or you'll face unpleasant surprises when filing year-end returns.

Passive Loss Carryforward Rules

Suspended passive activity losses from your S corp years generally carry over to your LLC. Whether you can actually use these losses depends on your entity classification and material participation going forward. The rules get technical here—LLC members face slightly different material participation tests than S corp shareholders in certain circumstances.

Costs and Timeline for S Corp to LLC Conversion

Understanding actual expenses and realistic timeframes helps you plan properly and avoid rushing through critical steps.

State Filing Fees Across Jurisdictions

Direct costs depend entirely on where you're registered. Budget-friendly states like Mississippi and Arkansas charge $50-$100 for complete conversion filing. Mid-tier states including Nevada, Illinois, and Texas run $150-$300. Expensive states like Massachusetts charge $500 just in filing fees, and California hits you with $70 for LLC formation plus that $800 franchise tax before you've earned any revenue.

| Where You're Converting | What You'll Pay | Processing Duration | Additional Requirements |

| Budget states | $50-$125 | 7-14 days | Basic conversion articles |

| Mid-range states | $150-$300 | 14-21 days | Conversion plan, possibly newspaper publication |

| Expensive states | $300-$520+ | 21-42 days | Detailed filings, tax clearance certificates |

| Publication-mandated states | Standard fees plus $200-$800 | Add 30 days | Legal notices in approved newspapers |

Professional Service Expenses

Most people hire professionals for conversion work. Attorney fees for preparing conversion documents, reviewing contracts, and ensuring proper filing typically run $2,000-$5,000 for straightforward conversions. Complex situations involving multiple properties, intellectual property portfolios, or creditors requiring special handling can push legal costs to $10,000 or higher.

Accountants charge $1,500-$3,500 for tax planning, basis calculations, and preparing final S corp returns. Businesses with complicated tax situations, multi-state filings, or significant built-in gains issues pay more for specialized tax guidance.

Hidden Costs Nobody Warns You About

Budget for expenses beyond obvious filing fees and professional services:

- License and permit updates: $50-$500 each

- Real estate retitling: $200-$1,000 per property depending on county recording fees

- UCC financing statement amendments: $25-$50 per filing

- Insurance policy endorsements: varies widely by coverage type

- Fresh bank accounts and check orders: $100-$300

- Updated signage, marketing materials, business cards: $500-$5,000 depending on what requires replacement

Realistic Timeframes

Plan on three to six months from initial decision to complete conversion:

- Planning and document preparation: 2-4 weeks

- Obtaining shareholder approval: 1-2 weeks

- State processing of your filings: 1-6 weeks (depends on state and whether you pay for expedited processing)

- License and permit updates: 2-8 weeks

- Contract amendments and securing third-party approvals: 2-12 weeks

- Final tax filings and wrapping up loose ends: 4-8 weeks

Most states offer expedited processing for $50-$500 extra, cutting state filing time down to 1-5 business days. Worth paying if you're in a hurry, but won't accelerate license transfers or contract amendments.

Alternatives to Converting Your S Corp

Before committing to conversion, consider whether other approaches might solve your problems more efficiently.

Simplify Corporate Procedures

Many problems people attribute to S corp structure actually stem from overly complicated internal procedures you've imposed on yourself. Try streamlining corporate formalities by:

- Scheduling board meetings only as frequently as legally required (often just annually)

- Using written consents instead of formal meetings when your state permits it

- Creating simple minute templates requiring 10 minutes to complete

- Allowing officers to make routine decisions without board approval for every minor item

These changes preserve S corp tax benefits while cutting administrative burden by 60-70%. You might solve your frustration without changing entity structure at all.

Author: Daniel Whitlock;

Source: worldwidemediums.net

Evaluate C Corporation Status

Converting c corp to llc is common, but some businesses discover C corp status works better under current tax law. The 21% federal corporate tax rate makes C corps attractive when you're retaining significant earnings for growth rather than distributing everything to owners annually. C corps also offer superior equity compensation tools—incentive stock options and employee stock purchase plans that LLCs cannot provide. If you're planning to pursue venture capital or eventually go public, C corp structure is essentially required.

Statutory Conversion Versus Dissolve-and-Reform

If your state offers statutory conversion, use it. The dissolution-and-formation method creates unnecessary complexity unless you have specific reasons requiring a fresh start. Statutory conversion preserves:

- Your original formation date (relevant for certain legal protections and priority rights)

- Existing contracts without needing assignment documents

- Licenses and permits without reapplication processes

- Legal continuity for pending lawsuits or claims

- Banking relationships without opening new accounts

Choose dissolution-and-formation only if your state lacks statutory conversion options or if you specifically need to shed certain liabilities or contractual obligations through the fresh start.

LLC Taxed as S Corporation

You can obtain LLC operational simplicity while keeping S corp tax treatment. Convert to LLC legal structure, then submit Form 2553 to have the LLC taxed as an S corporation. You maintain the salary-plus-distribution approach that minimizes self-employment taxes while gaining LLC flexibility in management and ownership. This hybrid approach works well for businesses valuing LLC simplicity but unwilling to pay thousands more annually in self-employment taxes.

Maybe Stay Put

Sometimes the best decision is maintaining your current structure. If administrative burden is your main complaint, streamlining internal procedures might fix it completely. If ownership restrictions concern you, evaluate whether those restrictions actually limit your real plans or just create theoretical problems you'll never actually face. Calculate the actual tax impact—if conversion would increase your self-employment taxes by $8,000 annually, staying as an S corp might be worth the extra paperwork and compliance costs.

Common Mistakes During S Corp to LLC Conversion

Learning from other people's expensive mistakes helps you avoid repeating them.

Failing to Notify Creditors

Many business owners overlook creditor notification requirements when changing entity structure. Loan agreements often give lenders rights to accelerate payment or modify terms when borrowers change legal form. Skip required notification and you could trigger default provisions even while making every payment punctually. Send formal written notice to everyone you owe money to, all landlords, and every party to long-term contracts at least 30 days before converting. Certified mail creates proof of notification if disputes arise later.

Improper Asset Transfer Documentation

When using the dissolution-and-formation method, some owners informally move assets to the new LLC without proper paperwork. This creates title problems (especially for real estate and vehicles) and can trigger unexpected tax consequences. Execute formal assignment agreements, bills of sale, and warranty deeds for every significant asset transfer. Record real property deeds with county recorders. File UCC amendments for any assets subject to liens or security interests. The few hundred dollars spent on proper documentation prevents tens of thousands in problems later.

Blowing IRS Deadlines

The IRS doesn't mess around with entity classification election deadlines. Submit Form 8832 more than 75 days after formation and it won't take effect until the following tax year. Form 2553 for S corporation election has identical strict timing requirements. Miss these deadlines and you're locked into default tax treatment for an entire year, potentially costing $5,000-$20,000 or more in additional taxes you could have avoided with timely filing.

Overlooking Publication Requirements

Several states mandate publishing conversion notices in local newspapers. Arizona requires three consecutive weekly publications in an approved paper. Nebraska mandates publication for three consecutive weeks. Forget publication requirements and you might invalidate the entire conversion or create ongoing liability exposure for LLC members. Don't assume the Secretary of State website lists every requirement—call their office directly to confirm publication rules in your jurisdiction.

Relying on Template Operating Agreements

Some owners convert using free operating agreement templates that don't address their specific situation. A poorly drafted operating agreement creates confusion about decision-making authority, profit distribution methods, and dispute resolution procedures. You'll spend far more fixing these problems later than you'd spend having an attorney customize an operating agreement upfront. A good operating agreement addresses your business's unique circumstances, ownership structure, and future plans rather than just filling in blanks on a generic form.

Ignoring Estimated Tax Payment Changes

Converting from S corp to LLC taxed as partnership completely changes your tax payment obligations. S corp owner-employees have taxes withheld from paychecks, reducing or eliminating estimated tax requirements. LLC members must make quarterly estimated tax payments covering both income tax and self-employment tax. Fail to adjust your estimated payments and you'll owe underpayment penalties when filing taxes. Set up your estimated payments on the conversion date, not when you discover you're short the following April.

Neglecting Employee Benefits and Plans

Converting entity structure affects employee benefit plans, retirement accounts, and employment agreements. ERISA plans might need amendments or complete restatement. Employment contracts that name the corporation specifically require updating to reflect the LLC. Workers' compensation policies need endorsements showing the new entity. Address these employment items systematically rather than discovering coverage gaps when an employee files a claim or tries to access retirement funds.

Frequently Asked Questions About S Corp to LLC Conversion

Converting from S corp to LLC means balancing operational preferences against tax considerations and administrative requirements. The process demands careful attention across legal filings, tax elections, and business relationship management.

Success depends on understanding your specific state's conversion procedures, documenting each step thoroughly, and addressing both federal and state tax implications. While reduced administrative burden and formality attract many owners to LLC structure, carefully evaluate whether benefits justify conversion costs and potential tax increases.

For businesses with substantial distributions where self-employment tax increases would exceed $10,000 annually, maintaining S corp status or electing S corp taxation for your LLC often makes better financial sense. For businesses prioritizing operational flexibility and simplified management, accepting higher self-employment taxes might prove worthwhile for the reduced compliance headaches.

Work with qualified legal and tax professionals who understand conversions to analyze your specific situation, calculate actual costs and tax impacts, and execute conversion properly. Professional guidance typically pays for itself by preventing mistakes and optimizing tax treatment.

Whether you convert or choose an alternative, base your decision on thorough analysis of your business's unique circumstances rather than general preferences or what worked for someone else's completely different business. The right entity structure aligns with how you actually operate, your ownership plans, and financial objectives while minimizing unnecessary complexity and cost.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Limited Liability Companies (LLCs), including formation, management, taxation, compliance, and business structuring.

All information on this website, including articles, guides, templates, and examples, is presented for general educational purposes. LLC requirements and regulations may vary depending on individual circumstances, business activities, state laws, and jurisdiction.

This website does not provide legal, tax, or financial advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.