Corporation owning one or more LLC entities in a business structure diagram

Can a Corporation Own an LLC?

Content

Content

Here's the short answer: absolutely. Every U.S. state permits corporations to hold membership stakes in LLCs. There's no special exception, no hidden rule that blocks this arrangement.

When your corporation becomes an LLC member, it works exactly like individual ownership—just with different paperwork. The corporation's legal name goes on the formation documents. Corporate officers sign agreements on behalf of the company. Your corporation receives profit distributions, votes on major decisions, and exercises control through whoever you've designated in your bylaws.

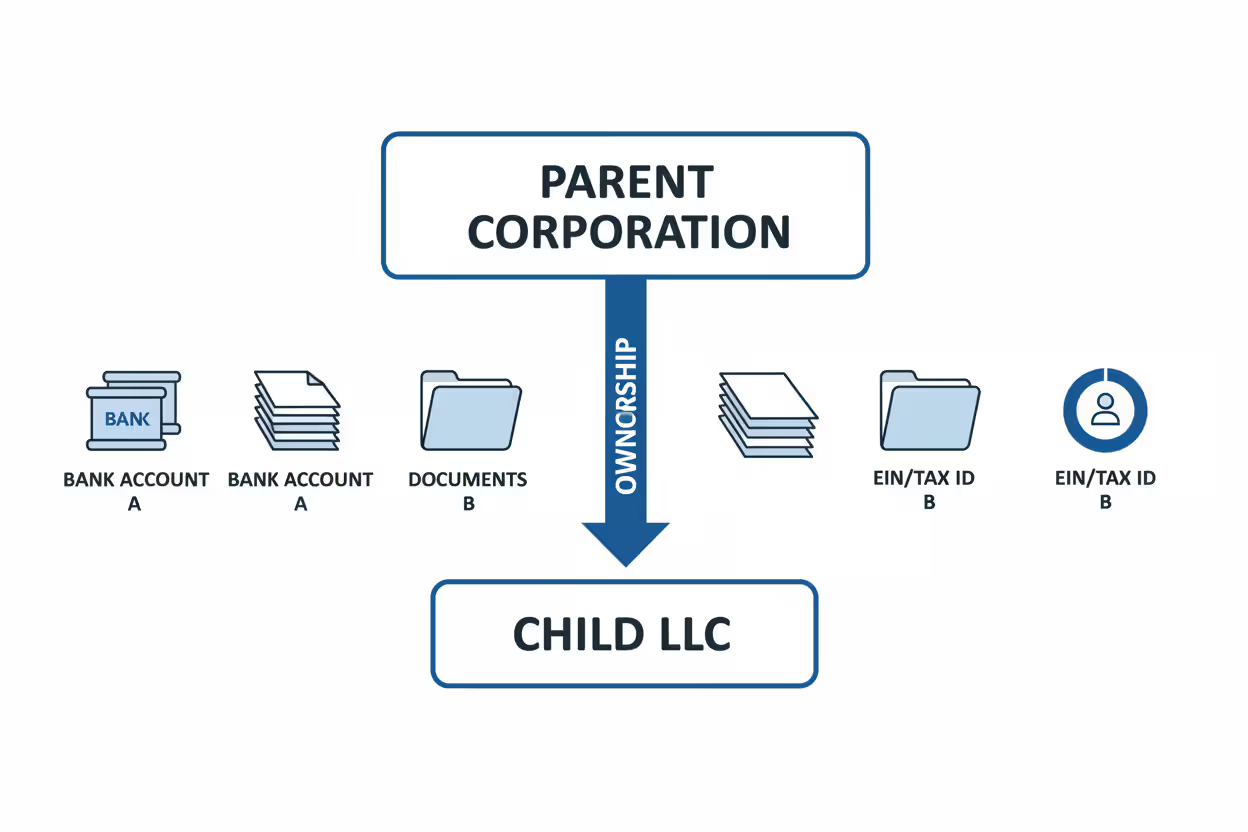

Think of it as creating a parent-child business relationship. The parent corporation owns the child LLC, but they remain separate legal entities. Each keeps its own employer identification number. Each files separately with the state (though tax filing depends on elections you make, which we'll cover later). Each maintains its own bank accounts and financial records.

Why does this flexibility exist? LLC statutes across states define eligible members as "any person," and here's the kicker—corporate law defines corporations as legal persons. That linguistic quirk opens the door for a corporate entity owns an LLC scenarios.

This setup differs fundamentally from mergers. Your LLC doesn't disappear into the corporation. Instead, it continues operating independently while the corporation holds the ownership interest. A restaurant corporation might own separate LLCs for each location. A consulting firm might create an LLC for a particular client contract. The possibilities extend as far as legitimate business purposes reach.

The corporation as llc member structure delivers something valuable: you get liability protection at two levels while keeping operational control centralized under the corporate umbrella.

Author: Kevin Halbrook;

Source: worldwidemediums.net

How a Corporation Becomes an LLC Owner

Before your corporation can own any LLC, your board of directors needs to vote on it. Draft a resolution explaining why this investment serves corporate interests, how much you'll contribute, and which officers have signing authority. Document this in your board meeting minutes—seriously, don't skip this step.

Buying into an existing LLC? You'll negotiate a purchase agreement with current members, then execute an assignment document transferring the membership interest to your corporation. Most operating agreements require existing members to approve new members, even when someone's buying their way in. Check the agreement first. Some allow unrestricted transfers, but that's the exception.

Starting fresh with a new LLC works differently. Your corporation becomes the organizer filing articles of organization with the secretary of state. List your corporation's full legal name exactly as registered, along with its jurisdiction of incorporation and entity number. The filing fee typically runs $50 to $500 depending on state.

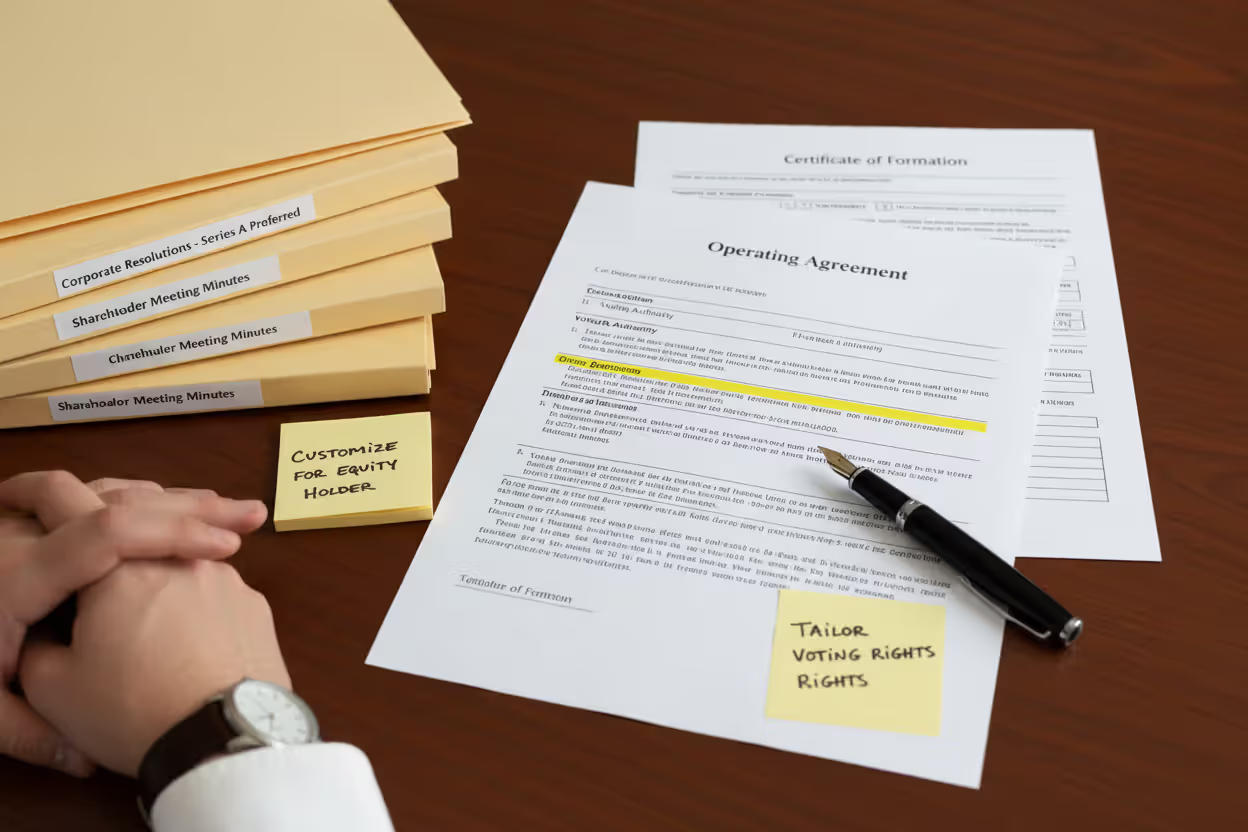

Now here's where people mess up: the operating agreement. Standard templates assume individual members who can personally attend meetings and vote. Your situation requires customization. Specify whether the corporation votes through formal board resolutions or delegates authority to a particular officer. Define how distributions get authorized. Clarify what happens if the corporation's ownership changes hands.

Author: Kevin Halbrook;

Source: worldwidemediums.net

The corporate owner llc relationship demands meticulous recordkeeping. Your corporation's balance sheet must list the LLC membership as an investment asset. Meeting minutes should reference major LLC decisions. Maintain separate ledgers showing which entity incurred which expense.

State quirks matter. California makes LLCs file a Statement of Information within 90 days of formation, listing all members including corporate ones. Delaware allows series LLCs—basically one master LLC containing multiple protected divisions—which corporations sometimes use for real estate portfolios. New York requires new LLCs to publish formation notices in two newspapers for six weeks, costing $1,000 to $2,000 in New York City.

Foreign corporations (meaning incorporated in a different state, not a different country) must qualify to do business in the state where they're forming or buying into an LLC. That means appointing a registered agent, filing a certificate of authority, and paying additional fees.

Why Corporations Choose to Own LLCs

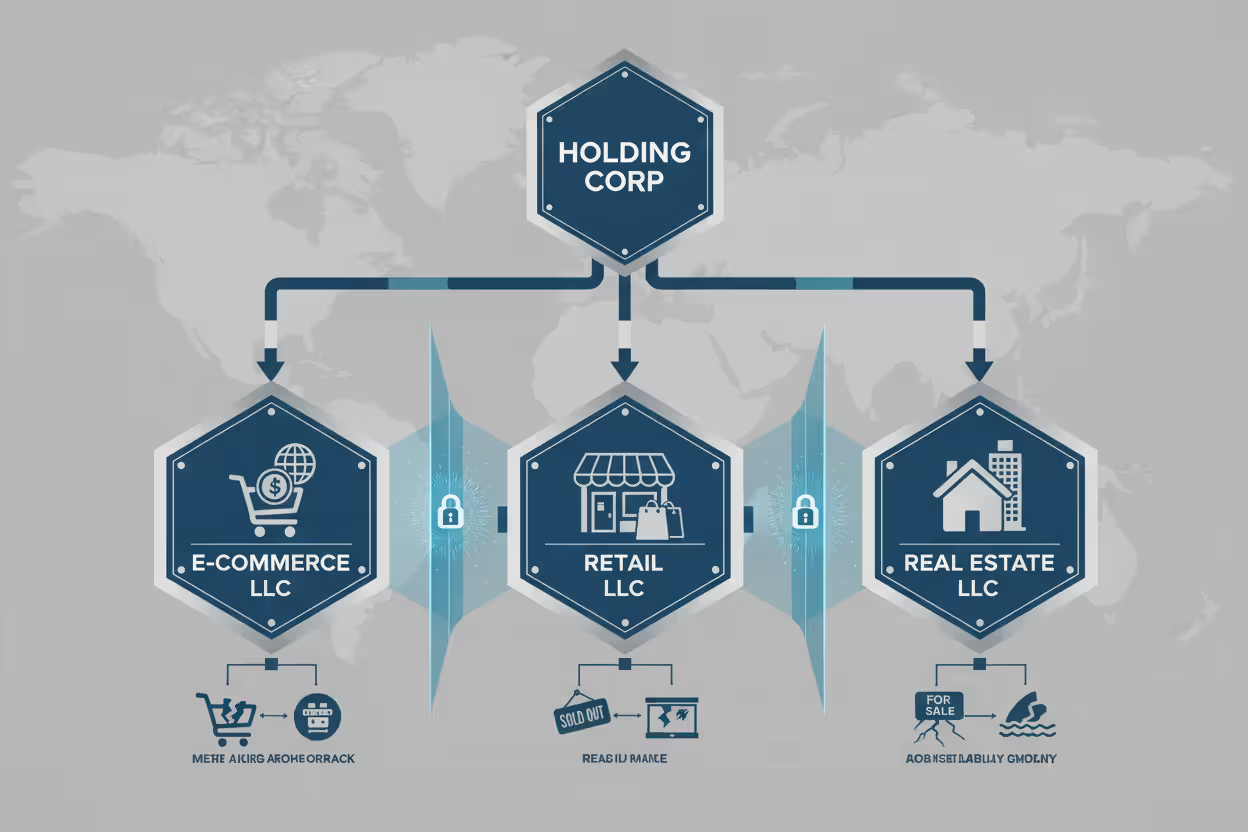

Asset segregation tops the list of reasons corporations pursue llc ownership by corporation arrangements. Let's say you run a successful retail corporation with $5 million in inventory and equipment. You're expanding into e-commerce, which carries cybersecurity risks your brick-and-mortar stores never faced. Create an LLC for the online division. Now if hackers breach customer data and lawsuits follow, plaintiffs can only reach the LLC's assets—not your entire retail operation.

Author: Kevin Halbrook;

Source: worldwidemediums.net

Real estate investors have turned this into an art form. One corporation owns ten LLCs, each holding a single commercial building. Tenant slips and falls in Building A? The lawsuit targets that property's LLC. Your other nine buildings remain untouchable. Even a massive judgment can't cross LLC boundaries to create liens on unrelated properties.

Joint ventures practically beg for this structure. Two corporations want to collaborate on a government contract but neither wants to merge or create a complicated partnership. Solution: form an LLC together, each corporation owning 50%. Write an operating agreement defining profit splits, decision-making authority, and exit procedures. When the project concludes, dissolve the LLC without untangling corporate ownership.

Tax planning motivates many arrangements, though you'd better understand the implications before proceeding (see the next section). Some corporations use LLC subsidiaries to shift income between entities in ways that reduce overall tax burden. Others consolidate financial statements while maintaining legal separation for liability purposes.

Subsidiary management gets easier with LLCs versus additional corporations. LLCs don't require annual shareholder meetings, boards of directors, or officer elections. Profit distributions can happen irregularly based on cash flow rather than formal dividend declarations. A corporation managing five subsidiary corporations faces fifty annual compliance tasks; managing five LLCs might require twenty.

Outside investment represents another strategic use. Your corporation wants funding for a new product line but won't dilute existing shareholders' equity in the parent company. Create an LLC for that product line, keep the corporation as majority owner, and sell minority stakes to investors. They get profit participation in the specific venture without governance rights over your core business.

Tax Implications When a Corporation Owns an LLC

C Corporation as LLC Owner

A C corporation owning a single-member LLC defaults to "disregarded entity" status with the IRS. What does that mean practically? The tax agency ignores the LLC's existence. All income and expenses get reported on the corporation's Form 1120 as if the LLC were just another division. The LLC keeps its EIN for employment tax purposes and certain excise taxes, but files no separate income tax return.

Here's the catch: profits still face the C corporation double tax trap. The LLC earns $100,000. That income gets taxed at 21% corporate rate (currently), leaving $79,000. When the corporation eventually distributes profits to shareholders as dividends, shareholders pay personal income tax on those distributions—potentially another 20% to 37% depending on their bracket. The LLC structure doesn't solve this problem; it just means LLC earnings contribute to corporate taxable income before distributions occur.

Some corporation owning an llc situations involve electing corporate taxation for the LLC by filing Form 8832. This creates two corporate tax layers, which sounds insane until you understand the scenarios. Maybe the LLC operates in a state with lower corporate tax rates, reducing combined state tax burden. Or you're planning to sell the LLC in five years, and corporate taxation creates basis step-ups that minimize capital gains on the sale.

Multi-member LLCs—where the corporation owns part but not all—default to partnership taxation. The LLC files Form 1065, allocates income and deductions among members, and issues K-1s. Your C corporation receives its K-1, reports that income on Form 1120, and pays corporate tax on its share. Partnership taxation adds complexity but enables special allocations (disproportionate profit splits) that straight corporate ownership can't achieve.

S Corporation as LLC Owner

S corporations can own single-member LLCs without problems, provided the LLC stays disregarded for tax purposes. The LLC's income flows to the S corporation's Form 1120-S, then passes through to shareholders via their K-1s. One layer of taxation—exactly what S corporations are designed to provide. The corporation as llc member arrangement doesn't disrupt pass-through treatment.

But watch out for multi-member LLCs. Here's where S corporations face a landmine. If the LLC has multiple members and defaults to partnership taxation, your S corporation becomes a partner in a partnership. Partnerships cannot own S corporation stock. The IRS treats partnership ownership as an ineligible shareholder, immediately terminating your S election.

The termination happens automatically on the date the S corporation acquires the LLC interest. Your S corporation becomes a C corporation retroactive to January 1st of that year. You owe back taxes reflecting the changed status. You can't make another S election for five years without IRS permission. It's a disaster.

The fix requires the multi-member LLC to elect corporate taxation via Form 8832 before the S corporation acquires its interest. Once the LLC is taxed as a corporation, it becomes either a qualified subchapter S subsidiary (if the S corporation owns 100%) or a regular corporate subsidiary that doesn't affect the parent's S status. You sacrifice pass-through taxation at the LLC level but preserve the S corporation's favorable treatment.

Many tax professionals tell S corporations to simply avoid LLC ownership unless there's a compelling reason. The risks of accidental S election termination, the complexity of maintaining proper elections, and the limited benefits compared to just operating divisions within the S corporation make this structure more trouble than it's worth in most cases.

Legal Considerations and Restrictions

State laws answer can a corporate entity own an llc with a resounding yes across the board, but nuances exist. Professional LLCs—for attorneys, doctors, accountants, architects, engineers—often limit membership to licensed practitioners. Unless your corporation itself holds the professional license (which most states only allow for professional corporations), you're blocked from ownership.

Operating agreements need provisions standard templates don't include. How does the corporation exercise voting rights—through board resolution each time, or by designating a permanent representative? What constitutes a transfer requiring other members' consent? If another company acquires your corporation, does that trigger transfer restrictions in the operating agreement? Who receives notices sent to members—the corporation's registered agent, CEO, or someone else?

Voting mechanics get tricky. Say your operating agreement grants voting proportional to ownership percentage, and your corporation owns 60%. Fine so far. But what if your corporation has three shareholders who disagree about how to vote the LLC interest? Does the corporation vote as a single block based on majority decision, or can it split its vote? Your operating agreement should specify this.

Bankruptcy concerns require planning. If your corporation files Chapter 11, can the bankruptcy trustee vote the LLC membership interest? Can the trustee sell the interest to fund the estate? Most operating agreements restrict transfers even in bankruptcy, but you need explicit language to avoid surprises.

Veil piercing becomes a dual concern with corporate owner llc structures. Creditors might try piercing the LLC veil to reach corporate assets, or pierce the corporate veil to reach shareholder assets. Courts look for red flags: commingled funds, inadequate capitalization, lack of formalities, using one entity's assets to pay another's obligations without documentation.

Maintain separation fanatically. Each entity needs its own bank account, used exclusively for that entity's transactions. When the corporation pays LLC expenses, document it as a capital contribution or loan with proper paperwork. When the LLC pays corporate expenses, same thing—document the transaction. Never "borrow" between entities informally.

Author: Kevin Halbrook;

Source: worldwidemediums.net

Compliance gets expensive. Your corporation files annual reports with its formation state. The LLC files annual reports with its formation state. If either operates in other states, they file foreign qualification documents and annual reports there too. Miss a filing and you risk administrative dissolution, which costs more to fix than preventing.

California hits both entities with an $800 annual minimum franchise tax. Own three California LLCs through your California corporation? That's $3,200 minimum before earning a dime. Delaware charges annual franchise tax based on authorized shares for corporations, plus $300 annual tax for each LLC. The fees add up faster than most business owners expect.

Corporation-Owned LLC vs. Other Ownership Structures

| Structure Type | Protection Level | Tax Approach | Complexity Factor | Formation Expense |

| Corp-owned LLC | Two-tier shield: LLC blocks claims against corp; corp blocks claims against shareholders | Varies by election: can be disregarded, partnership, or corporate | Substantial: dual compliance, separate formalities, coordinated governance | $500-$2,000+ for both entities |

| Individual owner | Single shield: LLC protects personal assets | Profits flow to owner's 1040 by default | Minimal: one set of records, sole decision-maker | $100-$500 for LLC only |

| Partnership members | Single shield: LLC protects partners | Profits allocated via K-1s to partners | Moderate: needs partnership agreement, coordinated management | $100-$800 including formation and agreements |

| Holding company model | Maximum isolation: parent owns nothing operational, just subsidiary interests | Highly flexible based on structure choices | Extensive: multiple entities each requiring compliance | $1,000-$5,000+ for multiple formations |

Individual ownership wins on simplicity. File once, decide alone, pay once. But you're exposed if someone successfully sues the LLC for more than it owns—they can pursue your personal assets through charging orders or other collection methods.

Partnership structures add coordination headaches without creating the double liability shield. Your LLC gets sued beyond its assets? Partner personal assets remain vulnerable despite the limited liability benefits most states provide.

Holding company arrangements—where a parent entity owns multiple subsidiary LLCs—deliver maximum protection. The parent holds only membership interests, no operational assets. Each subsidiary operates independently, isolating risks. A catastrophic loss at subsidiary #3 can't touch subsidiaries #1, #2, or #4. But maintaining this structure requires serious administrative commitment and professional fees.

I typically recommend corporate LLC ownership when clients already operate as corporations and face distinct risk categories they need to wall off. Real estate holdings, high-liability products, or expansion into new markets—these scenarios justify the added complexity. For corporations generating under $2 million annually, the administrative burden usually exceeds the benefits. Above that threshold, the asset protection and organizational clarity generally make the extra costs worthwhile

— Jennifer Martinez

Common Mistakes When Setting Up Corporate LLC Ownership

The number one error? Skipping the operating agreement or using a generic template without modifications. Business owners file articles of organization listing the corporation as member, then stop. Six months later when the LLC makes its first distribution, nobody knows how much to send or how the corporation should authorize receiving it. Disputes emerge. Lawsuits follow.

Tax election failures destroy value. An S corporation purchases 30% of an existing LLC for $200,000. Nobody checks whether the LLC is taxed as a partnership. It is. The S corporation's election terminates instantly. The owners discover this on April 15th the following year when their CPA prepares returns and realizes the S corporation became a C corporation last January. Fixing this requires private letter ruling requests costing $10,000+ in professional fees, assuming the IRS even grants relief.

Author: Kevin Halbrook;

Source: worldwidemediums.net

Commingling assets undermines everything. The corporation needs $5,000 to cover payroll. The LLC has cash sitting idle. Someone transfers money from the LLC account to the corporate account without documentation. Two months later it happens again. Pretty soon there's $50,000 of undocumented transfers flowing both directions. A creditor sues the LLC, tries to pierce the veil, discovers the commingling, and successfully argues the entities are alter egos of each other. Congratulations—you just lost both liability shields because you couldn't be bothered to document intercompany loans.

Inadequate capitalization screams "sham entity" to judges. Your corporation contributes $500 to form an LLC, which immediately borrows $300,000 to buy equipment. The LLC has no realistic ability to repay that debt from operations. Courts view this as using the LLC form to shield the corporation from liability while underfunding the entity actually conducting risky operations. When creditors come calling, judges often disregard the corporate structure in these scenarios.

Document contradictions create confusion. The articles of organization list the corporation as sole member. The operating agreement references three members with different ownership percentages. Which document controls? Are there actually three members or one? These inconsistencies suggest careless formation and undermine credibility when you claim the entities are legitimately separate.

Compliance calendars get neglected. Business owners remember to file the corporation's annual report but forget the LLC's deadline falls in a different month. The LLC goes into "not in good standing" status. Contracts become unenforceable. Late fees and reinstatement costs pile up. In some states, extended delinquency results in administrative dissolution requiring reformation from scratch.

Corporate records fail to reflect the LLC investment. The corporation's balance sheet shows no LLC asset. Board minutes contain no authorization to form or acquire the LLC. When examined during litigation or an audit, this looks like an individual officer conducting a personal side venture using corporate letterhead—not a legitimate corporate investment. The corporation owning an llc arrangement appears fabricated rather than real.

Frequently Asked Questions

Corporate ownership of LLCs works legally in every state and provides genuine strategic benefits for businesses needing asset protection, operational flexibility, and organizational structure. The arrangement isn't complicated conceptually—a corporation simply becomes an LLC member like any other owner.

Implementation demands attention to detail. You need proper authorization from your board, customized operating agreements addressing corporate ownership specifics, and tax elections that align with your goals. The dual-entity structure creates compliance obligations and costs that exceed simpler ownership models. You're maintaining two separate entities, each with its own filing deadlines, registered agent fees, and annual reports.

Tax implications shift dramatically based on whether you're a C corporation or S corporation, whether the LLC has single or multiple members, and which elections you make. S corporations face particular restrictions requiring careful navigation to avoid accidentally terminating their favored tax status. Professional tax guidance isn't optional—it's essential to avoid expensive mistakes.

Properly structured and maintained, corporate LLC ownership delivers meaningful liability protection and operational segregation. The protection depends entirely on treating both entities as genuinely separate—distinct bank accounts, separate financial records, documented decisions, and respect for the formalities justifying legal separation.

The structure makes most sense for established corporations with sufficient revenue to absorb the administrative costs and specific needs for asset segregation. A $500,000 annual revenue corporation probably shouldn't bother. A $5 million corporation segregating risky operations or valuable assets? That's when the benefits justify the complexity.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Limited Liability Companies (LLCs), including formation, management, taxation, compliance, and business structuring.

All information on this website, including articles, guides, templates, and examples, is presented for general educational purposes. LLC requirements and regulations may vary depending on individual circumstances, business activities, state laws, and jurisdiction.

This website does not provide legal, tax, or financial advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.