Investor desk with stock charts and LLC formation documents

How to Start an Investment LLC?

You've been trading stocks with your brother for three years now. The portfolio hit $400,000 last month. Your friend Janet wants in. Suddenly, that personal brokerage account feels uncomfortably exposed—what happens if someone sues? What if you disagree about selling that tech stock?

Here's where an investment LLC makes sense. It's not for everyone (definitely not if you're just dabbling with $10,000). But when you're pooling serious money or need protection, the structure works. Let's walk through exactly how to set one up.

What Is an Investment LLC

Think of it this way: an investment LLC is just a regular LLC that buys and holds investments instead of running a bakery or consulting business.

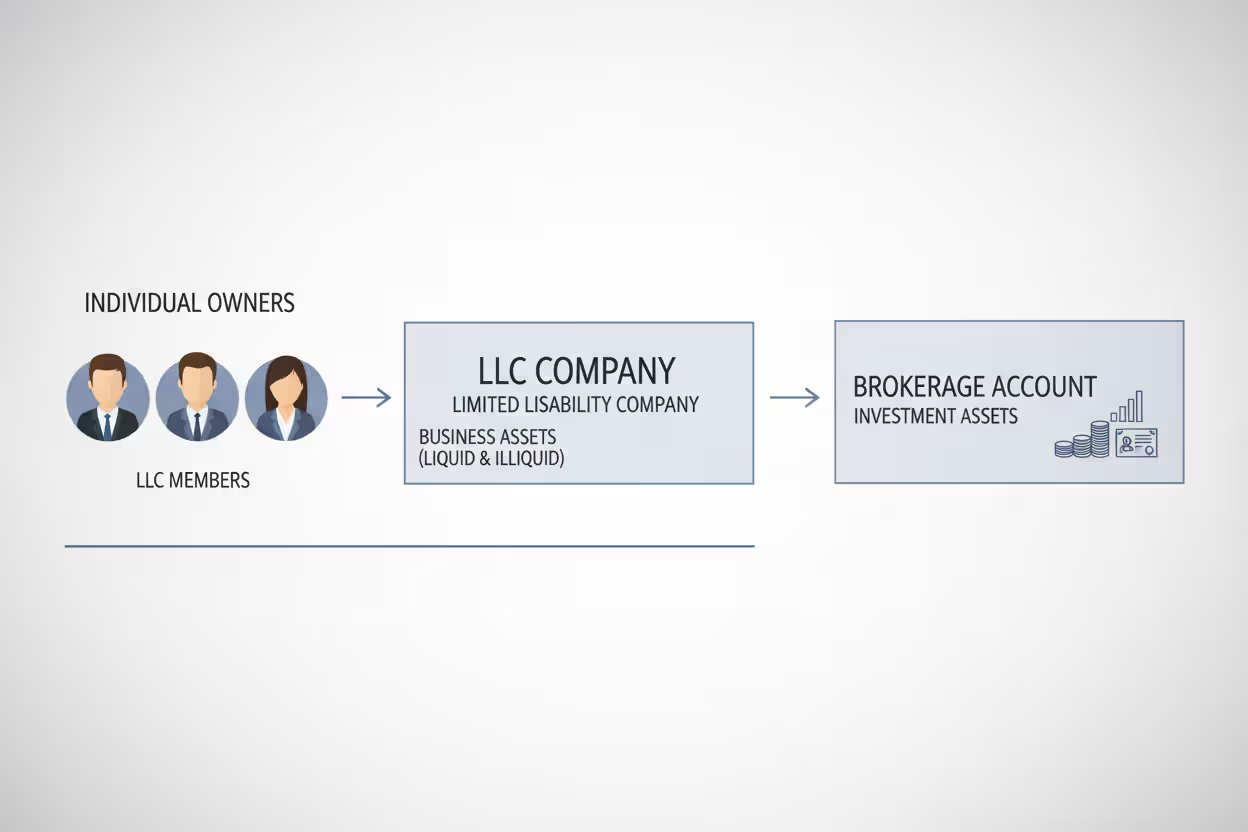

You're forming a legal company—registered with your state, with its own tax ID—that exists purely to own stocks, bonds, mutual funds, or other securities. The LLC's name goes on the brokerage account. The LLC owns the shares. You and your partners own the LLC.

Here's what actually matters: if something goes wrong with the investments, people generally can't come after your house. The LLC owns the losing position, not you personally. Your retirement account? Your car? Off limits in most cases (fraud and personal guarantees are different stories—we'll get to that).

Why not just use a corporation? Two reasons. First, corporations mean double taxation—the company pays tax, then you pay tax again on dividends. LLCs don't work that way. Profits flow straight through to your personal return. Second, S-corporations solve the tax problem but won't let you have foreign investors and cap you at 100 shareholders. LLCs? Way more flexible.

Partnerships sound simpler, sure. But in a general partnership, you're personally liable for everything—including your partner's dumb decisions. Limited partnerships help, but someone still has to be the general partner with unlimited liability. Nobody wants that job.

Author: Samantha Rowe;

Source: worldwidemediums.net

Investment LLC Structure and Ownership

You've got choices here, and they actually matter for how decisions get made and who pays what taxes.

Single-Member vs Multi-Member Investment LLCs

Single-member means exactly what it sounds like—you're the only owner. Maybe you've got $600,000 to invest and want liability protection. Or you're planning ahead for estate taxes. You form the LLC, you fund it, you keep all the profits.

Tax-wise? The IRS basically ignores it. They call it a "disregarded entity," which sounds insulting but just means you report everything on your regular 1040. No separate LLC tax return needed. Your Schedule D shows the capital gains just like always.

Bring in a second person—even your spouse in some states—and suddenly you're multi-member. Now you're filing a partnership return (Form 1065) every year and issuing K-1 forms. More paperwork, higher accounting fees.

But multi-member structures let you do interesting things. Your sister contributes $100,000 and gets 40% ownership. You put in $150,000 for 60%. Simple math. Or maybe you contribute less cash but you're doing all the research and trading, so the operating agreement gives you 50% anyway. Members can agree to split things however they want.

Manager-Managed vs Member-Managed Options

Member-managed is the default—everyone has equal say. All three partners can log into the brokerage, execute trades, sign contracts. Works fine when you're all active and aligned.

Manager-managed means you designate someone (or multiple people) to run things. Maybe your cousin joined for the creditor protection benefits but doesn't know stocks from socks. She's a passive member. You're the manager. You make the trading decisions, she gets her share of profits.

Your operating agreement needs to spell this out clearly. What requires a full member vote? Probably major things like borrowing money, changing investment strategy from value to crypto, or admitting new members. Day-to-day trades? Manager handles it.

I've seen LLCs fall apart because they skipped the operating agreement or grabbed some $29 template online. Don't. Spend the money for something customized. What happens when someone wants out? How do you handle one member getting divorced? Who breaks a tie vote? Address it now, not during a screaming match later.

Author: Samantha Rowe;

Source: worldwidemediums.net

Benefits of Forming an LLC for Investing

Let's be honest about what you're actually getting.

Liability protection is real but limited. Say your LLC buys options contracts that go spectacularly wrong. You lose the $200,000 in the LLC account. Painful, but creditors can't touch your personal savings. The separation holds.

It doesn't protect you from: anything you personally guaranteed (some margin agreements work this way), fraud or illegal activity (obviously), or situations where you mixed personal and LLC money so thoroughly a judge decides the LLC is fake.

Creditor protection works both directions. You personally get sued—car accident, professional malpractice, whatever. The plaintiff wins a judgment. Can they empty your LLC investment account? Usually no. Most states limit them to a "charging order," meaning they can collect distributions you actually receive but can't force liquidation or voting control. Makes the LLC interest less attractive than a regular bank account they could just drain.

Estate planning gets interesting with LLCs. You can gift shares to your kids annually while staying under gift tax limits. Better yet, because these are minority interests in a private company (your LLC), you can often claim valuation discounts—maybe 20-35% off the proportional value. So that 10% interest in an LLC worth $1 million might be valued at $700,000 for gift tax purposes.

The IRS has tightened up on aggressive discounts, though. You need proper appraisals and legitimate business purposes. Talk to an estate attorney, not your buddy who heard this trick at a seminar.

Privacy advantages exist in Wyoming, Delaware, and New Mexico—your name doesn't appear on public LLC filings. The LLC owns the brokerage account, not "John Smith." This won't hide assets from the IRS, divorce attorneys, or lawsuits where you're required to disclose holdings. But it does mean nosy neighbors can't just search state records.

Tax flexibility is mostly theoretical for investment LLCs. Yes, you could elect S-corp or C-corp status. Should you? Almost never. Those elections help operating businesses reduce self-employment tax. Investment income isn't subject to self-employment tax anyway. You'd just create problems.

Asset protection only works if you actually maintain it. First time you transfer LLC funds to your personal checking to cover your mortgage, you've pierced your own veil. Courts won't respect boundaries you ignore

— Michael Chen

How Investment LLCs Work for Stocks and Securities

Opening a brokerage account in your LLC's name involves more hassle than your personal account took.

You'll need: filed articles of organization, your EIN letter from the IRS, the operating agreement, and usually a written resolution saying you're authorized to open accounts and trade. Fidelity wants all of this. So does Schwab. Interactive Brokers. All of them.

Processing takes longer—figure two to three weeks versus twenty minutes for personal accounts. Some brokers set higher minimums for business entities ($10,000 isn't unusual). And certain features require extra approval. Want options level 3? Margin? You're filling out more forms about the LLC's investment experience and financial position.

The LLC becomes the legal owner. Every statement shows "Smith Family Investments LLC" as the account holder. You can't easily transfer stocks back and forth between your personal account and the LLC without creating taxable events. It's cleaner to fund the LLC with cash and buy positions fresh.

Here's where people mess up: securities regulations. You generally cannot advertise publicly for investors, accept money from unlimited numbers of people, or operate like a mini mutual fund without triggering Investment Company Act registration requirements. The most common exemption limits you to 100 beneficial owners and prohibits general solicitation.

Family LLCs—parents and adult kids pooling money—almost never hit these issues. Start accepting money from colleagues or neighbors? You might need securities counsel. The SEC doesn't care about your trading activity. They care intensely about how you raise capital.

Author: Samantha Rowe;

Source: worldwidemediums.net

Steps to Set Up an Investment LLC

Here's the actual process, step by step.

Choose your formation state. Unless you have specific reasons otherwise, use your home state. I know you've heard Delaware is the gold standard. For a three-person investment LLC in Ohio? Delaware just means you pay Ohio and Delaware fees, file reports in both states, and gain essentially nothing.

Wyoming offers charging order protection even for single-member LLCs—that's unusual. Nevada has no state income tax. These might matter for your situation. But the "incorporate in Delaware" advice comes from corporate law contexts that don't apply to small investment groups.

Name your LLC. Check availability on your Secretary of State's website. You need "LLC" or "Limited Liability Company" somewhere in the name. Can't use "Bank" or "Insurance" without licenses. Keep it simple—"Martinez Family Investments LLC" works better than "Quantum Capital Synergy Partners LLC."

File articles of organization. This is usually a two-page form online. LLC name, registered agent address, management structure (member or manager-managed), and organizer name. Processing ranges from same-day (if you pay $100+ for expedited service) to two weeks for standard filing.

Wyoming charges $100. Massachusetts wants $500. California only charges $70 to file but hammers you with $800 annual minimum tax later. Check your state's fee schedule.

Obtain an EIN. Go to IRS.gov, click "Apply for an EIN Online," answer the questions. Takes ten minutes. You get the number immediately. Don't pay someone $200 to do this for you.

Draft an operating agreement. Your state probably doesn't require filing this, but you absolutely need one. Cover:

- Initial capital contributions (who's putting in what)

- Ownership percentages (might differ from contributions)

- Profit and loss allocation (usually matches ownership, but doesn't have to)

- Voting rights and manager authority

- Investment strategy boundaries (are we doing only index funds? Including crypto? Max 20% in any single stock?)

- Addition of new members

- Withdrawal and buyout procedures

- Death or divorce of a member

Generic templates miss investment-specific issues. What happens if members disagree about rebalancing? Who has authority to establish new brokerage accounts? Spend $800-1,500 for an attorney to customize this.

Open business bank and brokerage accounts. Get a checking account first—local bank or credit union is fine. You need somewhere for members to send contributions and to pay LLC expenses (state fees, accounting costs).

Then tackle the brokerage account. Gather all formation documents. The broker will want to verify your EIN, review the operating agreement, and confirm who's authorized to trade. If you want multiple authorized traders, specify that clearly.

Fund the LLC. Members write checks or wire transfer their capital contributions to the LLC checking account. Record everything—date, amount, member name. Then move the money to the brokerage account and start investing.

Don't skip the recordkeeping step. I've seen LLCs where nobody could remember who contributed what. That's a disaster waiting for tax season.

Author: Samantha Rowe;

Source: worldwidemediums.net

Tax Treatment and Reporting Requirements

This confuses people more than it should.

Pass-through taxation means the LLC itself doesn't pay federal income tax. Your investment gains, dividend income, interest—everything flows through to members' personal returns. The LLC is essentially transparent for tax purposes.

Single-member LLC? You report it all on your own 1040. Schedule D for capital gains, Schedule B for interest and dividends, same as if you owned the stocks personally. No separate LLC return.

Multi-member LLC? Now you file Form 1065 partnership return showing all income and expenses. Then you prepare a Schedule K-1 for each member showing their share. Each member reports their K-1 amounts on their personal return. You're not being taxed twice—you're just documenting how the shared income splits between partners.

Self-employment tax doesn't apply here, and that's important. If you formed an LLC to run a consulting business, your profits would get hit with 15.3% self-employment tax (Social Security and Medicare). Investment income is passive—it doesn't get self-employment tax whether you own the investments personally or through an LLC.

Some people elect S-corp status to reduce self-employment tax. Makes zero sense for investment LLCs since you're not paying it anyway. You'd just add complexity and S-corp restrictions for no benefit.

Capital gains treatment passes through unchanged. Your LLC buys Tesla stock and holds it for two years. Sells for a $40,000 gain. You get long-term capital gains rates (probably 15%) on your share of that $40,000. Same as if you'd owned the Tesla shares directly.

Short-term gains—positions held under a year—flow through as ordinary income, just like normal.

State taxes vary wildly. Texas has no income tax but charges franchise tax on LLCs with revenue over $1.23 million (investment income counts). California charges $800 minimum annually plus a fee based on gross receipts—can easily hit $5,000+ for profitable LLCs. New York has a filing fee that scales from $25 to $4,500 based on member count and income.

Florida, Wyoming, and Nevada have no income tax and minimal fees. Research your specific state before forming.

Corporate tax elections exist but rarely make sense. You could elect S-corp or C-corp treatment. Why would you? S-corp status helps service businesses pay less self-employment tax—irrelevant here. C-corp status creates double taxation—terrible for investments. Stick with default pass-through unless your CPA has extremely compelling reasons.

Costs and Ongoing Compliance

Let's talk real numbers, because formation is only the beginning.

Initial formation fees by state:

| State | Filing Fee | Annual Report/Tax | Registered Agent (Annual) |

| Wyoming | $100 | $60 | $100-300 |

| Delaware | $90 | $300 | $100-300 |

| Nevada | $425 | $350 | $125-350 |

| Florida | $125 | $138.75 | $100-300 |

| Texas | $300 | $0* | $100-300 |

| New York | $200 | $9-4,500** | $100-300 |

| California | $70 | $800+ | $100-300 |

| Montana | $70 | $20 | $100-300 |

Texas has franchise tax for LLCs over revenue threshold

*New York fee scales with LLC size

Registered agent fees run $100-300 annually if you hire a service. Or $0 if a member agrees to serve as agent. The registered agent needs a physical address in your formation state (not a P.O. box) and must be available during business hours to accept legal papers.

Using yourself saves money but puts your home address on public record. Commercial services provide privacy and won't miss important deadlines because you were on vacation.

Operating agreement preparation costs $500-1,500 with an attorney, or $0-200 for online templates. I've already beaten this drum, but investment LLCs have unique needs. That $49 LegalZoom template written for consulting businesses won't address rebalancing authority, risk tolerance disagreements, or how to handle a member wanting to withdraw capital mid-year.

Accounting and tax preparation adds $500-2,500 annually. Single-member LLC with buy-and-hold index funds? Maybe $300-500 above what your personal return already costs. Multi-member LLC with active trading across options, bonds, and international stocks? Expect $1,500-2,500 for partnership return, K-1 preparation, and individual return complications.

Annual state fees range from $0 (Texas and Montana don't charge annual report fees) to $800+ in California plus potential gross receipts fees. Budget for this recurring expense—it's easy to forget about the June registered agent bill or October state franchise tax.

When does this make financial sense? Rough guideline: below $100,000 in assets with simple strategies, probably not worth it. Between $100,000-250,000, it's borderline—depends heavily on your liability concerns and state costs. Above $250,000 with multiple members or substantial leverage? Usually worth the structure.

Common Mistakes When Starting an Investment LLC

Learn from others' expensive errors.

Undercapitalization means forming an LLC with $500, then immediately transferring in $800,000 of securities. Courts look at this and see a sham—you're not treating it like a real business entity. Contribute reasonable starting capital relative to your investment plans. A few thousand dollars minimum shows legitimate purpose.

Commingling funds destroys liability protection faster than anything else. Using LLC accounts to pay your personal electric bill? Depositing LLC dividends to your personal checking? Congratulations, you just taught a judge that your LLC separation is fake. They'll "pierce the corporate veil" and let plaintiffs access your personal assets.

Maintain absolute separation. LLC money stays in LLC accounts. Personal expenses come from personal accounts. Yes, it's annoying to maintain separate checking accounts and credit cards. Do it anyway.

Poor record-keeping bites you during lawsuits or IRS audits. Document your decisions—even single-member LLCs should keep written notes about major choices. Track every capital contribution and distribution with dates and amounts. Save all brokerage statements and tax documents for at least seven years.

The time to organize records is not when you're being sued.

Ignoring securities laws happens when cousin Bob wants to invest $50,000 and you figure, "Why not?" Then his friend hears about it. Then his friend's neighbor. Suddenly you've got eight investors, you posted about it on LinkedIn, and the SEC is asking uncomfortable questions about unregistered securities offerings.

Family investment LLCs with parents and adult children? Generally fine. Accepting money from friends, colleagues, or strangers? You need securities counsel first. Private placement exemptions have strict rules about advertising and investor qualifications.

Wrong state selection wastes money. That $2,000 online course promised Delaware LLCs would save you thousands in taxes. You live in Michigan. You're now paying Delaware annual fees ($300), Michigan foreign LLC registration and fees, and getting zero actual benefit. Formation tourism rarely helps small investment LLCs.

Skipping the operating agreement because Kansas doesn't require it seems smart until you and your sister stop speaking. Who decides whether to sell the rental property REIT? What happens when she wants her capital back but you think it's a terrible time to liquidate positions? Default state law probably won't match what you intended.

Using personal brokerage accounts after forming your LLC means your protection is theoretical, not real. The LLC must legally own the investments—meaning the brokerage account title must show the LLC as owner. Assets you personally own don't get LLC protection just because an LLC exists.

Author: Samantha Rowe;

Source: worldwidemediums.net

FAQ

Investment LLCs work when your situation needs them. Multiple people pooling significant capital? Yes. One person investing $50,000 in index funds? Probably not.

The structure delivers real liability protection, creditor insulation, and estate planning flexibility. You get pass-through taxation without corporate complexity. But you're accepting state filing requirements, higher accounting costs, and ongoing administrative discipline.

Figure $1,000-2,000 to set up properly, then $500-2,500 annually to maintain. Worth it for a three-sibling LLC managing a $600,000 inherited portfolio. Overkill for your personal $40,000 Robinhood account.

Before forming an investment LLC, honestly assess your situation. Do you have liability exposure worth protecting against? Multiple investors requiring formal structure? Enough assets to justify the expenses? If you're checking these boxes, an LLC makes sense.

Talk to an attorney familiar with your state's LLC law and a CPA who handles investment entity taxation. They'll tell you whether your specific circumstances warrant the structure—and help you avoid the expensive mistakes people make when they try to DIY everything after watching a YouTube video.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Limited Liability Companies (LLCs), including formation, management, taxation, compliance, and business structuring.

All information on this website, including articles, guides, templates, and examples, is presented for general educational purposes. LLC requirements and regulations may vary depending on individual circumstances, business activities, state laws, and jurisdiction.

This website does not provide legal, tax, or financial advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.