Small business owner reviewing LLC and S corp tax options at a desk

Single Member LLC Taxed as S Corp Guide

Content

Content

You've built a profitable single-member LLC, and every April you're watching a significant chunk of your earnings disappear to taxes. Maybe your accountant casually mentioned S corporation elections during last year's tax prep. Or perhaps a business owner in your network won't stop talking about their tax savings. Now you're wondering if you're leaving money on the table.

Here's the reality: changing your LLC's tax classification could reduce your annual tax burden by five figures—but that savings comes with payroll obligations, compliance requirements, and administrative costs that make some owners wish they'd never heard of S corporations. Some entrepreneurs pocket an extra $12,000 yearly. Others discover they're spending more on compliance than they're saving in taxes.

This guide breaks down exactly what you're getting into and whether the math actually works for your situation.

Understanding S Corp Tax Treatment for Single Member LLCs

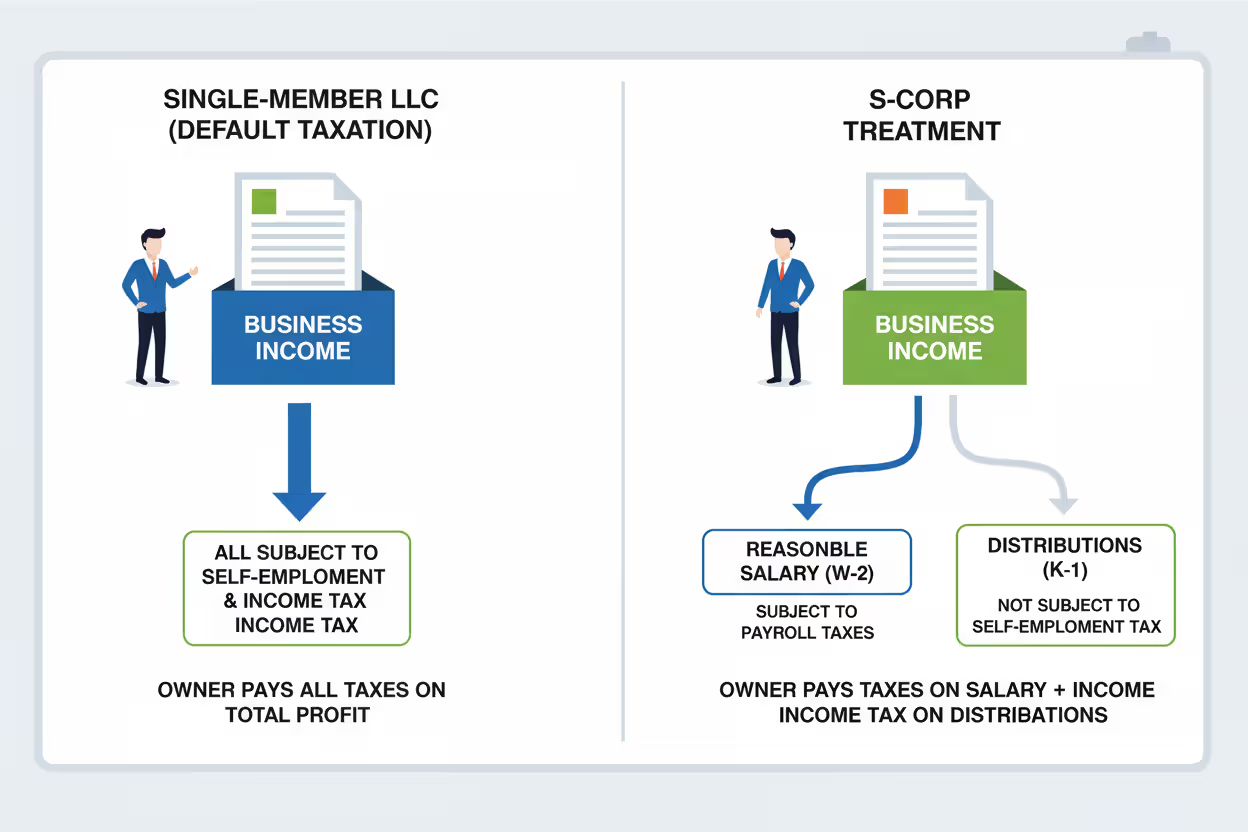

Your single-member LLC currently operates as what tax professionals call a "disregarded entity"—the IRS essentially pretends your business doesn't exist as a separate taxpayer. You report all income and expenses directly on Schedule C of your personal tax return. Every dollar of profit gets classified as self-employment income, subjecting you to 15.3% self-employment tax covering Social Security and Medicare contributions, plus your regular income tax rates.

When you elect S corporation tax treatment, you're fundamentally restructuring how the IRS views your income—without touching your LLC's legal status. Your state government still recognizes you as a limited liability company. Your operating documents don't change. Your business name stays identical. The legal entity remains exactly what it was.

Author: Kevin Halbrook;

Source: worldwidemediums.net

The transformation happens entirely at the tax level. Under S corp treatment, the IRS recognizes you in dual roles: as both an employee performing work and as an owner receiving profits. You must establish formal payroll and compensate yourself a regular salary with standard tax withholdings—federal income tax, Social Security, and Medicare. This salary component still faces the full 15.3% employment tax burden. The difference appears in what happens next: remaining profits flow to you as owner distributions, which completely bypass that 15.3% self-employment tax.

This creates an obvious temptation to minimize your salary and maximize distributions. The IRS anticipated this move decades ago. Federal tax law requires "reasonable compensation"—you must pay yourself what a qualified person would typically earn for performing your actual job duties. Underpay yourself substantially, and you're essentially inviting IRS scrutiny, potential reclassification of your distributions as wages, and penalties that eliminate any tax advantage.

This reasonable compensation requirement explains why S corp election only makes financial sense above certain profit thresholds. Imagine your LLC generates $45,000 in annual profit, but reasonable compensation for your role runs about $38,000. You're only saving 15.3% on $7,000—approximately $1,071. That won't cover the costs of operating payroll, much less the additional accounting fees.

Your business now files Form 1120-S, the S corporation return, instead of reporting everything on Schedule C. You receive a Schedule K-1 documenting your ownership share of income (100% in your case). The corporation itself pays zero federal income tax—profits still pass through to your personal return just like before. The critical difference is that mandatory split between wage compensation and ownership distributions.

Filing for S Corporation Tax Status with Your Single Member LLC

Form 2553, "Election by a Small Business Corporation," handles this election. Despite the technical-sounding title, it's actually a straightforward two-page form.

The deadline drives everything else. Planning to begin S corp treatment on January 1st? Your Form 2553 must reach the IRS no later than March 15th—miss this cutoff by a single day and you're waiting until the following year. The IRS maintains a rigid deadline: the election must arrive within two months and fifteen days after your tax year begins.

Recently formed LLCs get different treatment. Submit Form 2553 within two months and fifteen days of creating your LLC, and the election becomes immediately effective. Create your LLC on August 10th, file the election by October 25th, and you're operating as an S corp for tax purposes for the remainder of that calendar year.

The form requests basic information: your LLC's legal name as registered with your state, Employer Identification Number, chosen tax year, and your requested effective date. You'll sign as the sole member. Here's where things trip up many filers: you must already have an EIN before submitting Form 2553. Some entrepreneurs reverse this sequence—submitting the election first, then applying for an EIN afterward. That's backwards and causes rejection.

The signature section generates constant issues. Unsigned submissions get automatically rejected, as do forms containing incorrect or missing EINs. Another frequent problem: filing the form successfully but never actually implementing payroll. Once the IRS accepts your S corp election, they expect to see corresponding W-2s and quarterly employment tax returns. Skip these requirements, and you've created a compliance nightmare even though your election technically went through.

What happens if you missed the cutoff? The IRS provides late election relief for taxpayers who can demonstrate "reasonable cause." This typically requires attaching a detailed statement explaining what prevented timely filing and demonstrating it wasn't deliberate disregard. File within three years and seventy-five days of your target effective date, and the IRS might grant relief. I've seen situations where clients missed deadlines due to medical emergencies or natural disasters—the IRS accepted these with proper documentation.

After mailing Form 2553, expect a sixty-day wait. The IRS typically responds within this window, either approving your election or requesting additional information. When that approval notice arrives, safeguard it carefully. You'll need this documentation if audit questions arise or when demonstrating your tax classification to state revenue departments.

Author: Kevin Halbrook;

Source: worldwidemediums.net

Tax Advantages of Choosing S Corp Status for Your Single Member LLC

The core benefit boils down to simple arithmetic: avoiding 15.3% self-employment tax on a portion of your profit. Let's examine actual scenarios.

Suppose your LLC generates $120,000 in net income this year. Under default LLC taxation, you're facing roughly $18,130 in self-employment tax. (The actual calculation applies 15.3% to $118,500 because you deduct half the SE tax first, but that's technical detail.)

Now consider the same $120,000 under S corp treatment. You establish a reasonable salary of $60,000. This $60,000 portion still carries full payroll tax—approximately $9,180. The remaining $60,000 flows to you as ownership distributions, completely avoiding the 15.3% self-employment tax. You've just saved roughly $9,180 in taxes.

Hold on, though. Payroll processing services cost you $1,200 annually. Your accountant charges an additional $1,500 for preparing Form 1120-S instead of simple Schedule C. Your actual net savings drops to $6,480. Still meaningful, but nowhere near the full $9,180.

Determining reasonable compensation keeps business owners awake at night. The IRS publishes no formulas, safe harbors, or clear guidelines. They simply state your compensation should align with what "the marketplace would bear" for similar work. A web developer earning $180,000 who pays herself $35,000 is practically begging for IRS attention. What's appropriate? Possibly $75,000 to $95,000 depending on your regional market and experience level.

Your industry dramatically affects reasonable compensation. An attorney generating $300,000 in revenue requires substantially higher reasonable salary than a retail business owner with identical revenue but completely different profit margins and job responsibilities.

Here's how the numbers compare across different profit levels:

| Total Business Profit | SE Tax Under Default LLC Treatment | Reasonable Salary Amount | Payroll Tax Under S Corp | Distribution Received | Estimated Tax Savings |

| $50,000 | $7,065 | $35,000 | $5,355 | $15,000 | $1,710 |

| $100,000 | $14,130 | $55,000 | $8,415 | $45,000 | $5,715 |

| $150,000 | $18,228 | $75,000 | $11,475 | $75,000 | $6,753 |

Numbers reflect current tax rates with Social Security wage base of $168,600. Estimated savings exclude payroll service fees, increased accounting costs, and administrative time.

Distribution timing offers operational flexibility too. Your salary must remain consistent—you can't arbitrarily start and stop payroll. Distributions work differently. Take them monthly, quarterly, or whenever cash flow permits. Experiencing a challenging quarter? Skip the distribution. Just received a major client payment? Take a distribution immediately. This flexibility helps when you're purchasing equipment, building inventory, or simply managing irregular cash flow.

Author: Kevin Halbrook;

Source: worldwidemediums.net

Disadvantages and Expenses of S Corporation Tax Elections

Running payroll for yourself creates an absurd-feeling situation initially. You're paying yourself, withholding from your own paycheck, and remitting your own tax payments to government agencies. And you're paying a service provider to facilitate this circular transaction.

Payroll services typically charge $40-$150 per month, totaling $500-$1,800 annually. Some accounting firms include payroll in their service packages. Others bill separately for payroll administration. Regardless of the arrangement, it's a new recurring expense in your budget. You could process payroll yourself using software, but then you're dedicating hours to payroll calculations, tax deposits, and quarterly filings rather than generating revenue.

Speaking of accounting fees, expect a significant increase. Form 1120-S requires considerably more work than Schedule C. Your accountant needs to track basis adjustments, document reasonable compensation decisions, and maintain corporate formalities. Where you previously paid $800 for straightforward LLC tax preparation, you're now looking at $1,500-$3,000 for the S corp return combined with your personal filing.

Quarterly filings become routine. Form 941—the employer's quarterly payroll tax return—documents wages paid and taxes withheld every three months. Miss a quarter or file after the deadline? Penalties start at $250 and escalate quickly. The IRS treats payroll tax compliance seriously because these represent trust fund taxes withheld from employee wages.

State tax treatment introduces unexpected complications. California imposes an $800 annual minimum franchise tax on all S corporations regardless of profitability. Tennessee assesses an excise tax on S corp income. New York City maintains its own S corporation tax system. Meanwhile, Texas doesn't recognize S corp elections at all—they tax based on gross receipts regardless of federal classification.

Certain states even treat S corp distributions as self-employment income anyway, completely eliminating your federal tax savings. Before submitting Form 2553, invest time researching your specific state's approach to S corporations. That research might reveal thousands in savings or expose that the entire strategy fails in your jurisdiction.

The election makes zero sense for marginally profitable businesses. Suppose you netted $35,000 last year. Reasonable compensation might run $28,000, leaving $7,000 for distributions. You save 15.3% on $7,000—about $1,071. Your payroll service costs $1,200 annually. You're actually losing money on this strategy before considering higher tax preparation fees.

Product-based businesses often struggle with increased compliance demands. When you're juggling inventory management, tracking cost of goods sold, and handling variable monthly income, adding payroll complexity might overwhelm your systems. Service businesses with predictable income and strong margins typically find S corp elections much simpler to manage.

Planning to raise capital or bring on partners? S corporations cannot have corporate shareholders, partnership owners, or non-resident aliens. They're restricted to a single class of stock, complicating preferred stock arrangements that investors frequently require. You might elect S corp treatment today only to revoke it in eighteen months when your growth plans exceed these limitations.

Author: Kevin Halbrook;

Source: worldwidemediums.net

Required Tax Filings for Single Member LLC S Corps

Your compliance calendar just expanded dramatically. Here's what a complete year looks like.

March 15th marks the Form 1120-S deadline. This S corporation tax return reports all business income, deductions, and credits. Unlike typical tax returns, it doesn't calculate tax liability—S corporations don't pay federal income tax. Instead, the return generates Schedule K-1, documenting your proportionate share of income, deductions, and credits that transfer to your personal return.

April 15th brings your personal return deadline—Form 1040, which incorporates that K-1 from your S corporation. The business income appears on your 1040, you calculate and pay tax on it, completing the pass-through taxation cycle.

Between these annual deadlines, quarterly obligations accumulate. Form 941 comes due April 30th, July 31st, October 31st, and January 31st. Each filing reports your salary, withheld federal income tax, and Social Security and Medicare taxes. You're also making federal tax deposits throughout every quarter—some businesses deposit semi-weekly, others monthly, depending on cumulative tax liability.

Year-end involves W-2 preparation. You'll issue yourself a W-2 documenting your annual salary and withholdings, identical to what traditional employers provide. That W-2 gets transmitted to the Social Security Administration by January 31st using Form W-3. Your state revenue department likely requires copies as well.

State and local requirements multiply these obligations. Quarterly wage reports, unemployment insurance filings, state-level payroll tax returns—each jurisdiction maintains unique requirements and deadlines.

Reasonable salary documentation deserves careful attention. You need to demonstrate your methodology. How did you arrive at $65,000 or $80,000 or whatever figure you chose? Gather salary surveys from the Bureau of Labor Statistics. Save job postings for comparable positions in your region. Document your actual responsibilities, hours committed, and professional qualifications. When the IRS questions your compensation decisions, you need contemporaneous documentation demonstrating it was reasonable when established—not justification you manufactured after receiving an inquiry.

Shareholder basis tracking sounds technical but carries real consequences. Your basis begins with your initial LLC investment. It increases when the business generates profit and decreases when you receive distributions. Take distributions exceeding your basis? Those convert to capital gains, taxed at rates you didn't anticipate. Want to deduct a business loss? You can only deduct losses up to your basis amount. Many owners completely ignore basis until facing unexpected tax consequences.

Maintain meticulous records separating salary payments from ownership distributions. Document the date and amount of every distribution. Track each payroll execution, every tax deposit, every business expense. The IRS expects corporate-level formality even though you're operating solo. Commingle personal and business spending, or fail to properly document distributions, and you risk losing both S corp tax benefits and your limited liability protection.

Author: Kevin Halbrook;

Source: worldwidemediums.net

Determining If S Corp Election Fits Your Single Member LLC

Your net profit largely dictates the answer. Generating under $60,000 in net profit? The compliance expenses probably exceed your tax savings. Consistently clearing $100,000? You should absolutely model the numbers carefully. The $60,000 to $80,000 range represents gray area where appropriateness depends entirely on individual circumstances.

Service professionals typically receive the clearest benefits. If you're a consultant, freelance professional, designer, or other service provider with minimal overhead and healthy margins, S corp election frequently delivers meaningful savings. You've got predictable income, limited equipment expenses, and straightforward bookkeeping. Adding payroll doesn't substantially complicate your existing operations.

Product sellers, manufacturers, and retail businesses often find less benefit. Thinner profit margins mean less potential savings. Inventory complexity and variable income make payroll administration more burdensome. The administrative overhead might not justify modest tax savings.

I generally suggest clients evaluate S corp election around $75,000 in profit, though I've encountered situations where it made sense at $50,000 and others where waiting until $100,000 was wiser. It depends heavily on state tax treatment, existing payroll infrastructure, and frankly, your capacity for managing complexity. I've worked with clients who saved $8,000 on taxes but experienced such stress about payroll compliance they ultimately revoked the election. Don't just analyze spreadsheets—consider your actual life circumstances and business reality

— Jennifer Martinez

Business trajectory matters as much as current earnings. Generating $55,000 currently but projecting $120,000 next year? Establishing the election now builds your systems and processes before entering rapid growth. Income oscillating between $40,000 and $90,000 year over year? Compliance burdens during lean years might outweigh savings during profitable periods.

Consider where you're taking this business. Planning to sell within five years? S corp classification can complicate transactions depending on deal structure. Bringing on a partner soon? You'll need to assess whether S corp ownership restrictions create obstacles. Converting to C corporation for venture capital? That transition from S corp to C corp triggers tax consequences requiring advance planning.

Your personality and resources factor significantly. Hate administrative tasks? Already overwhelmed managing daily operations? Adding payroll, basis tracking, and corporate record-keeping might push you past your breaking point. Working with a bookkeeper and accountant who efficiently handle these requirements? The burden decreases substantially.

Risk tolerance plays a role too. The IRS scrutinizes S corporation reasonable compensation more aggressively than almost any other tax issue. Choose an aggressive compensation strategy—paying yourself well below market rates to maximize distributions—and you're substantially increasing audit risk. Prefer sleeping well at night? Perhaps stick with straightforward LLC taxation even if it costs you some tax dollars.

Common Questions About Single Member LLC S Corp Elections

Electing S corporation taxation can substantially reduce your tax obligation once your single-member LLC consistently generates above $60,000-$80,000 in annual profit. The self-employment tax savings are genuine and meaningful at higher income levels.

You're exchanging simplicity for those savings, though. Payroll administration, additional tax filings, reasonable salary documentation, and corporate formalities all demand time, money, and attention. Miss payroll tax deadlines, establish unreasonably low compensation, or skip mandatory filings, and you'll incur penalties that eliminate any potential savings.

Before submitting Form 2553, calculate realistic savings using market-appropriate salary figures for your position. Subtract all compliance expenses—payroll services, increased accounting fees, and your time commitment. Research your state's specific approach to S corporation taxation. Consider whether the administrative requirements suit your working style and business operations.

Consult with a CPA or tax professional experienced in your industry and state. Have them model scenarios using your actual financial data rather than generic examples. The correct decision depends on your specific profit levels, business type, growth trajectory, and personal tolerance for administrative complexity. For certain businesses, S corp election represents an obvious choice saving thousands yearly. For others, it's an expensive complication that never generates positive returns.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Limited Liability Companies (LLCs), including formation, management, taxation, compliance, and business structuring.

All information on this website, including articles, guides, templates, and examples, is presented for general educational purposes. LLC requirements and regulations may vary depending on individual circumstances, business activities, state laws, and jurisdiction.

This website does not provide legal, tax, or financial advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.