Small business owner reviewing LLC and S corporation tax documents in an office

How an LLC Taxed as S Corp Works?

Content

Content

Walk into any small business accounting office in January, and you'll hear the same conversation a dozen times: "Wait, I paid how much in self-employment tax?" That shock often leads to discovering S corporation election—a tax strategy that's been around since 1958 but still surprises LLC owners every year. The mechanics aren't complicated: you split your income into two buckets (wages and distributions), pay employment taxes on only one bucket, and pocket the difference. Sounds simple until you factor in the IRS paperwork, payroll headaches, and state-by-state quirks that come with it.

What It Means When an LLC Is Taxed as an S Corp

The IRS views your LLC as invisible for tax purposes when you first set it up. A one-owner LLC gets treated like you're just self-employed (Schedule C on your 1040). Multiple owners? The IRS sees a partnership and wants Form 1065. Either way, you're writing a check for 15.3% self-employment tax on everything the business earns after expenses.

Here's where llc taxed as an s corp comes in. You're not dissolving your company or creating a new entity. The legal structure—your Articles of Organization, your state registration, your EIN—all stay exactly the same. You're just asking the IRS to tax you differently by submitting Form 2553 (Election by a Small Business Corporation). Think of it like choosing how you want your paycheck calculated, except the choice affects thousands of dollars annually.

After the IRS approves your election, you wear two hats: employee and owner. The employee hat means cutting yourself actual paychecks with tax withholding, just like you would for hiring someone. The owner hat means taking what's left over as distributions—money that bypasses the 15.3% employment tax hit. You'll file Form 1120-S each year instead of Schedule C, and you'll get a K-1 showing your share of profits.

Your operating agreement doesn't vanish when you make this election. Neither does your LLC's liability shield or management flexibility. What changes is the IRS's perspective on how your money gets categorized and taxed. This distinction matters when banks, clients, or lawyers ask about your business structure—you're still an LLC in every legal sense.

Author: Daniel Whitlock;

Source: worldwidemediums.net

Benefits of LLC Taxed as S Corp

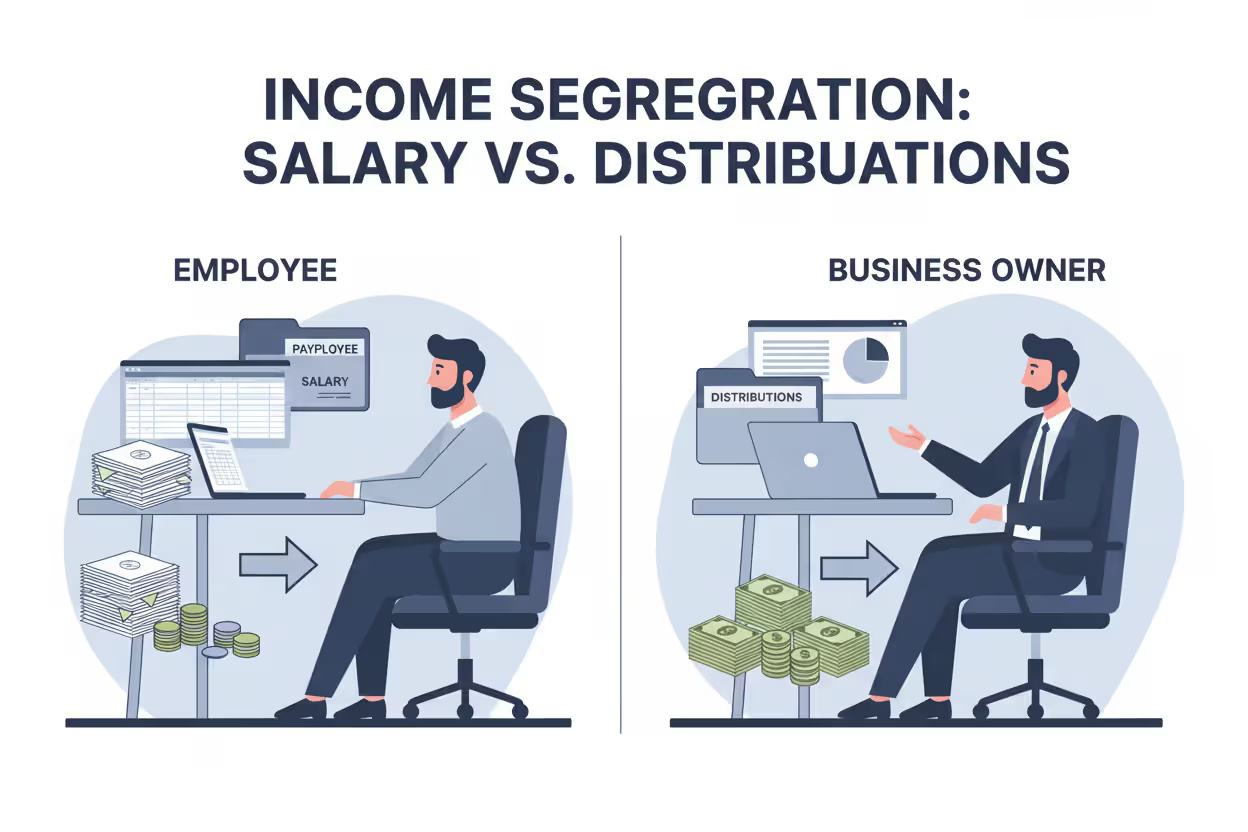

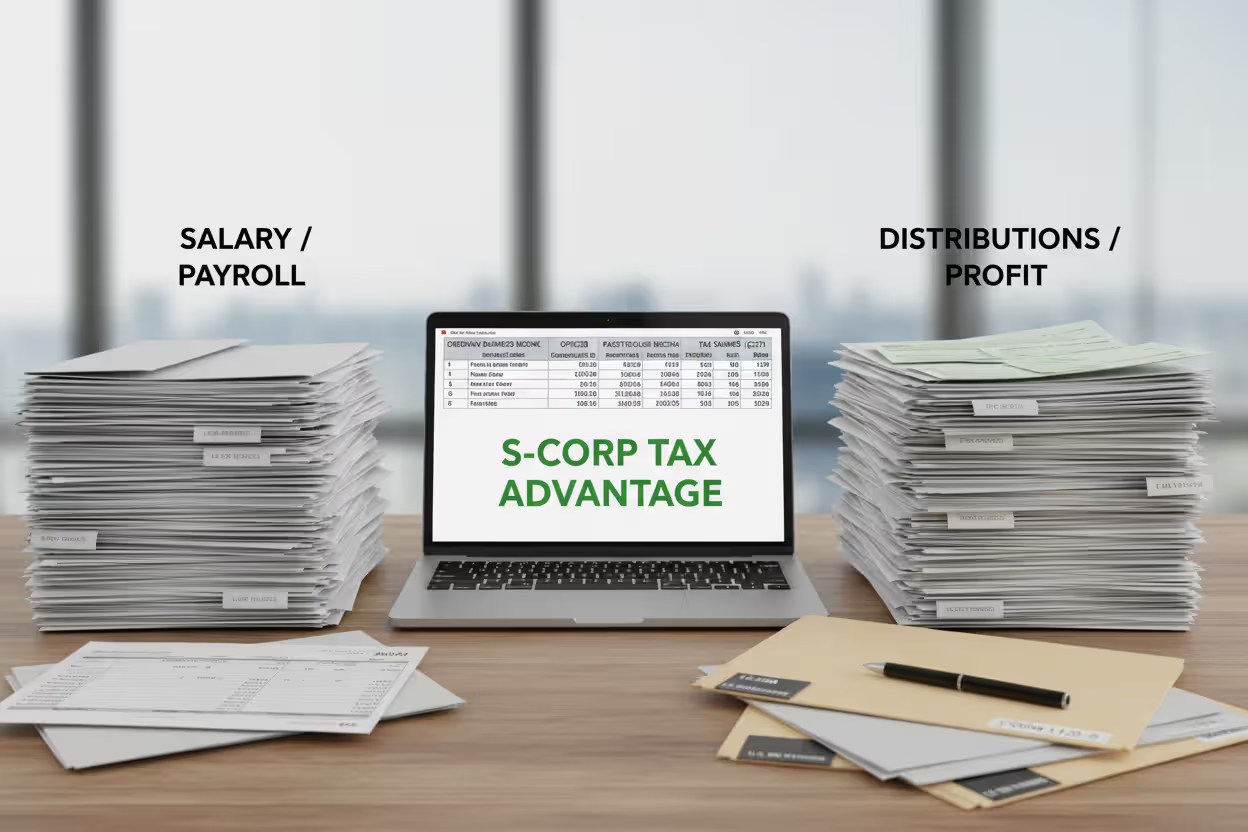

Self-employment tax savings create the biggest draw. Under standard llc s corp taxation versus default treatment, every profit dollar gets hit with Social Security (12.4% up to the wage base) and Medicare (2.9% on everything, plus 0.9% on higher incomes). When you're pulling $100,000 from your business, that's $15,300 gone before income tax even enters the picture.

Switch to S corp treatment, and watch what happens. You set your salary at $65,000 (we'll cover "reasonable" in a minute). You take $35,000 as distributions. Now you're paying employment taxes on $65,000, not $100,000. That's roughly $5,355 in immediate savings, year after year.

Pass-through taxation stays put, which matters more than people realize. C corporations face double taxation—the company pays tax on profits, then shareholders pay tax on dividends. S corporations skip that first layer entirely. Your business income lands on your personal return via Schedule K-1, taxed once at your individual rate. This structure has survived since the Eisenhower administration because it works.

The salary-distribution split gives you planning leverage. Let's say you land a massive contract in December. You could delay distributions until January, pushing that income into next year's tax return. Your salary stays consistent (because the IRS watches for games), but distribution timing offers legitimate flexibility. Contrast this with default LLC taxation, where every dollar you earn hits your return immediately whether you actually withdraw it or not.

Your LLC's liability protection continues unchanged because you haven't touched the legal entity. Members still can't be personally liable for business debts or lawsuits (assuming you maintain formalities). Some entrepreneurs worry that changing tax treatment somehow pierces the corporate veil—it doesn't. State law governs liability protection; federal tax elections don't override it.

One underrated advantage: certain clients and contracts require corporate status. Government RFPs sometimes specify "corporation" without clarifying whether that includes LLCs. S corp taxation doesn't make you a corporation legally, but the 1120-S filing and corporate tax treatment satisfy some procurement departments that would otherwise disqualify you.

Author: Daniel Whitlock;

Source: worldwidemediums.net

Requirements and Eligibility for S Corp Taxation

The IRS caps S corporation ownership at 100 people. Each person must hold U.S. citizenship or permanent residency—green card holders qualify, but someone on a work visa doesn't. The shareholder list can't include other corporations, LLCs, or partnerships. If you've brought in an investor who operates through their own LLC, you'll need to restructure before electing S status.

The one-class-of-stock rule creates headaches for LLCs with creative profit splits. Everyone's ownership must carry identical distribution and liquidation rights. You can structure different voting rights (Class A votes on major decisions, Class B doesn't), but the economic rights must match ownership percentages. If your operating agreement gives one member a preferred return or guaranteed payments, you've created a second class of stock, disqualifying your election.

Reasonable salary remains the IRS's favorite audit trigger. They don't publish a chart saying "Your salary must be X% of distributions," but they've litigated enough cases to establish patterns. Take David Watson, the Watson PC case from 2012: he paid himself $24,000 while taking $175,000 in distributions. The Tax Court reclassified most distributions as wages, adding $50,000 in back taxes and penalties. The IRS looks at industry comparables—what would you pay someone with your skills and responsibilities? A developer billing $150/hour can't justify a $30,000 salary. An accountant generating $250,000 in revenue can't get away with $40,000 wages.

Compliance obligations multiply once you elect. You're now running payroll, which means:

- Calculating and depositing federal withholding every pay period (or monthly/quarterly depending on amounts)

- Filing Form 941 four times per year reporting wages and taxes

- Submitting Form 940 annually for federal unemployment tax

- Issuing W-2s by January 31st

- Preparing Form 1120-S and K-1s for all shareholders

- Making quarterly estimated tax payments on your distribution income

Author: Daniel Whitlock;

Source: worldwidemediums.net

States treat llc taxed as an s corporation wildly differently. California recognizes the election but charges a 1.5% tax on S corporation income exceeding $250,000. New Hampshire ignores it completely and taxes your business as an LLC regardless. New York City imposes its own S corporation tax on top of state obligations. Texas has no income tax, so the election affects only federal returns. Check your state's Department of Revenue website before assuming federal election equals state recognition.

Operating Agreement Modifications for S Corp Taxation

Most LLC operating agreements handle money distribution based purely on ownership stakes and member votes. That setup can conflict with S corporation requirements in subtle ways.

A sample operating agreement for llc taxed as s corporation needs provisions addressing salary before distributions. Here's language that works: "Members who actively participate in company operations shall receive compensation reflecting the fair market value of their services. Compensation levels shall be reviewed annually and adjusted to remain consistent with industry standards for similar roles and responsibilities." This creates documentation supporting your reasonable salary defense if questioned.

The distribution section needs tightening. Standard LLC agreements often include discretionary distribution clauses like "Distributions shall be made at times and in amounts determined by the Manager." That's fine for default taxation but problematic for S corps. Add this: "All distributions shall be allocated among members in direct proportion to their ownership interests. No member shall receive distributions that would violate the one-class-of-stock requirement under Internal Revenue Code Section 1361(b)(1)(D)."

Terminology shifts cause real confusion when your operating agreement discusses "members" and "membership interests" while your 1120-S refers to "shareholders" and "stock." You don't need to replace every instance—instead, add a tax status provision: "The Members intend for this Company to be taxed as an S corporation under Subchapter S of the Internal Revenue Code. For all federal tax purposes, 'members' shall be treated as 'shareholders,' 'membership interests' shall be treated as 'shares of common stock,' and this Agreement shall be interpreted consistently with maintaining S corporation election eligibility."

Key additions your agreement should cover:

- Compensation approval process: Which member (or what percentage vote) sets salary amounts and reviews them

- Distribution frequency and mechanics: Quarterly? Annual? Who authorizes each distribution?

- Transfer restrictions: Preventing transfers to ineligible shareholders (foreigners, corporations, etc.)

- Tax item allocation: Confirming income, deductions, and credits flow proportionately

Sample clause for maintaining eligibility: "No member may transfer any interest in the Company to any person or entity that would cause termination of the Company's S corporation election, including but not limited to nonresident aliens, corporations, partnerships, or ineligible trusts. Any attempted transfer violating this restriction shall be void."

You don't need to scrap your entire operating agreement and start over. Most attorneys recommend an amendment specifically addressing S corp requirements, which runs $500-1,200 depending on complexity. The amendment supplements your existing agreement rather than replacing it—you're adding guardrails, not rebuilding the whole structure.

Author: Daniel Whitlock;

Source: worldwidemediums.net

Drawbacks and When S Corp Election Doesn't Make Sense

Payroll processing alone costs $40-150 monthly if you outsource it. ADP, Gusto, and Paychex all offer small business packages, but you're still looking at $500-1,800 per year. Your accountant will charge more to prepare Form 1120-S than Schedule C—expect an additional $600-2,500 for tax prep. State filings add another $100-500 depending on location. Total additional annual costs typically land between $1,500-4,500 before factoring in your time.

That time commitment isn't trivial. Payroll runs on a schedule—biweekly or semi-monthly for most businesses. You can't just move money from business to personal checking when you need groceries. Each payroll cycle requires calculating withholding, submitting tax deposits (late deposits trigger penalties starting at 2% and climbing to 15%), and maintaining documentation. Miss a quarterly 941 filing? The IRS charges 5% of unpaid taxes per month, maxing out at 25%.

The math stops working below certain profit levels. If your LLC nets $45,000, you might save $4,000 in self-employment tax. Subtract $2,500 in compliance costs, and you're left with $1,500—barely worth the hassle. The breakeven point hovers around $60,000-75,000 for most businesses, though it varies based on your specific costs and tax situation.

Several scenarios make llc taxed as an s corporation the wrong choice:

- Loss years: When your business loses money, those losses offset your other income. S corporation loss deductions are limited by your basis (capital contributions plus loans you personally made to the business). LLC members often claim larger deductions because their basis includes the LLC's debts—something called "debt basis" that S corps don't offer.

- Real estate rentals: Rental income isn't subject to self-employment tax already. Adding S corp complexity generates zero savings while creating extra filing requirements and potential state-level tax hits.

- Retaining profits for growth: If you're reinvesting 80% of earnings back into inventory, equipment, or expansion, you'll face phantom income problems. You owe income tax on your share of profits even if you didn't take distributions. Now you need to extract distributions just to pay the tax bill, which defeats the purpose of retaining capital.

- Foreign ownership or entity partners: The moment you bring in an investor who's not a U.S. citizen or who invests through their own company, your S election terminates immediately. That triggers five years before you can re-elect.

The Section 199A qualified business income deduction adds another layer. You can claim up to 20% of qualified business income as a deduction whether you operate as a default LLC or an S corp. The catch: S corporation owners calculate QBI on their K-1 income minus W-2 wages. Sometimes that results in a smaller deduction than default taxation would provide. Running projections both ways before electing can reveal that the QBI deduction advantage under default taxation exceeds the self-employment tax savings from S corp status.

How to Elect S Corp Status for Your LLC

Business owners read a blog post about S corp savings and file Form 2553 without understanding what they're committing to," Rodriguez explains. "Six months later, they haven't run a single payroll, they're moving money around randomly, and they're shocked when I tell them they're facing penalties. The tax savings are real—I've helped clients save $15,000-30,000 annually—but only when net income exceeds $75,000 and the owner can handle consistent payroll processing. If you're not prepared to treat yourself like an employee with regular paychecks and tax withholding, don't elect S corp status. The compliance requirements aren't suggestions

— Michael Rodriguez

Form 2553 itself spans three pages and requires information about your LLC, tax year, and all members. Every single member must sign the consent section, or you must attach a separate consent statement. You'll need your EIN, formation date, and details about each member's ownership percentage and acquisition date.

The March 15 deadline catches people off guard. To have S corporation status apply to this calendar year, your Form 2553 must reach the IRS by March 15. File on March 20th, and you're generally looking at waiting until January 1st of next year for the election to take effect. The IRS does offer late election relief under Revenue Procedure 2013-30, but you must demonstrate "reasonable cause" and you must have been operating as if the election were in place (running payroll, filing 1120-S, etc.). They approve most requests, but why risk it?

Some LLCs need to complete a two-step process. If your multi-member LLC has been operating for years, you might need Form 8832 to elect corporate classification before submitting Form 2553 for S corporation status. Single-member LLCs and newly formed LLCs can usually go straight to Form 2553, but unusual timing situations require checking the instructions carefully.

State elections operate independently in many jurisdictions. Filing Form 2553 with the IRS doesn't automatically notify your state. California requires filing Form 100-S. Illinois wants Form IL-1120-ST. Some states have no separate form but require checking a box on your first S corporation return. A handful of states (Tennessee, for instance) simply don't recognize S corporations at all for state tax purposes—your federal election has zero impact on your state return.

Step-by-step filing process:

- Confirm eligibility check: Review the shareholder count, citizenship status, ownership structure, and one-class-of-stock requirement

- Operating agreement review: Identify conflicts between current provisions and S corp rules

- Get universal consent: Have all members sign Form 2553 Part I or provide separate consent statements

- Complete Part I: Basic company information and election effective date

- Complete Part II: Each shareholder's information and consent signature

- Complete Part III: Only if needed for late election relief

- Submit to IRS: Mail to the address listed in instructions for your state, or fax to (855) 641-6935

- File state election: Submit required state forms within their deadlines

- Establish payroll system: Set up withholding, deposit schedules, and quarterly reporting before issuing first paycheck

- Restructure bookkeeping: Create separate accounts tracking salary expense versus distributions

Author: Daniel Whitlock;

Source: worldwidemediums.net

Working with a qualified CPA or tax attorney isn't legally required but proves valuable. They'll model whether S corp election makes sense given your specific income level, state situation, and business type. Initial consultations run $300-1,000. Full election assistance including form preparation, state filings, and first-year setup guidance costs $1,000-2,500. That seems expensive until you consider that filing errors, missed deadlines, or unreasonable salary decisions can trigger IRS notices resulting in $5,000-20,000 in back taxes and penalties

Comparison of LLC Default Taxation vs. LLC Taxed as S Corp

| Feature | LLC Default Taxation | LLC Taxed as S Corp |

| Tax Treatment | Schedule C for single-member; Form 1065 for multi-member | Form 1120-S with Schedule K-1 issued to each owner |

| Self-Employment Tax | 15.3% applies to entire net profit amount | Only applies to W-2 salary; distributions escape it |

| Payroll Requirements | None—owners take draws as needed | W-2 payroll mandatory; quarterly Form 941 filings; annual Form 940 |

| Administrative Burden | Minimal—attach Schedule C or file partnership return | Substantial—payroll processing, corporate tax return, K-1 preparation, quarterly obligations |

| Best For | Startups, businesses netting under $60,000, rental properties, situations with foreign owners | Established operations with consistent $75,000+ profit and capacity for payroll compliance |

FAQ

Choosing S corporation taxation for your LLC makes financial sense once your business reaches a specific profit threshold—usually $75,000 or higher in stable net income. The ability to categorize income as salary (subject to employment taxes) versus distributions (escaping the 15.3% hit) creates immediate savings. You maintain pass-through taxation avoiding double taxation, keep your LLC's liability protection intact, and gain some tax planning flexibility around distribution timing.

The strategy demands commitment to ongoing compliance work. Payroll processing becomes non-negotiable. Quarterly filings and annual tax forms multiply. Costs increase by $1,500-4,500 annually before counting your time investment. For businesses netting under $60,000 or operating in states hostile to S corporations, these burdens often exceed the benefits.

Before submitting Form 2553, calculate your potential savings against your specific compliance costs. Review your operating agreement for necessary amendments—transfer restrictions, distribution rules, and salary provisions all need addressing. Verify you meet every IRS eligibility requirement: shareholder limits, citizenship rules, and the one-class-of-stock mandate. Understand that reasonable salary isn't optional—it's the IRS's primary audit focus for S corporations.

Consider hiring a CPA or tax attorney for the initial election and first-year compliance. The upfront cost ($1,000-2,500) protects you from mistakes that trigger back taxes and penalties often exceeding $10,000. They'll model whether S corp election makes sense for your situation, handle the filing process correctly, establish proper payroll procedures, and create systems preventing future compliance failures. The tax savings compound year after year, but only if you execute the strategy properly from day one.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Limited Liability Companies (LLCs), including formation, management, taxation, compliance, and business structuring.

All information on this website, including articles, guides, templates, and examples, is presented for general educational purposes. LLC requirements and regulations may vary depending on individual circumstances, business activities, state laws, and jurisdiction.

This website does not provide legal, tax, or financial advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.