Small business tax planning workspace with LLC documents and laptop

Self Employment Tax LLC Guide for Business Owners

Most LLC owners discover an expensive surprise during their first tax season: they're paying way more in taxes than they expected. Here's what happens—you form your LLC, thinking you've set up the perfect business structure, then your accountant drops the bomb that you owe 15.3% on top of your regular income tax.

The frustrating part? Your LLC's legal structure (which protects your personal assets) operates independently from how the IRS taxes your business. You could have two identical LLCs earning the same revenue, and one owner might pay $15,000 more in taxes simply because they made different elections when setting up their tax treatment.

Your tax bill depends on choices you make—choices many business owners don't even realize they're making. Should you stick with default tax treatment, or file paperwork to be taxed differently? That decision alone can shift thousands of dollars between your pocket and the Treasury's.

What Is Self-Employment Tax and How Does It Work

Here's the situation business owners face: employees and their employers each kick in 7.65% toward Social Security and Medicare. That's 15.3% total going to fund these programs. When you run your own business, you're wearing both hats—you're simultaneously the worker and the boss. The IRS expects you to pay the entire 15.3% yourself.

This 15.3% divides into two buckets. Social Security grabs 12.4% of your earnings up to $168,600 in 2026. Once you cross that threshold, the Social Security portion stops. Medicare takes 2.9% with no ceiling—you'll pay it on every dollar you earn. Earn above $200,000 individually or $250,000 jointly? Another 0.9% gets added through the Additional Medicare Tax.

Here's where it gets confusing: you're dealing with two completely separate tax calculations. Income tax varies based on your total earnings and tax bracket—anywhere from 10% up to 37% in 2026. Self-employment tax gets calculated first, before you even determine what you owe in income taxes. You end up paying both taxes on identical earnings.

Author: Olivia Carrington;

Source: worldwidemediums.net

The IRS does throw you one bone: you calculate self-employment tax on 92.35% of your business profit, not the full amount. Why 92.35%? It's meant to mirror the benefit employees get (since their employers pay half the tax, employees aren't taxed on that compensation). Picture earning $100,000 profit from your business. You'll actually calculate self-employment tax on $92,350. Still expensive, but slightly less painful than the full amount.

Do LLCs Pay Self-Employment Tax

Here's the truth nobody tells you when you're forming your LLC: the IRS doesn't care that you created a limited liability company. They don't have a tax box labeled "LLC." Your LLC is invisible to them until you tell them how you want to be taxed.

By default, the IRS assigns your tax treatment based on how many members your LLC has. Single owner? They'll treat you exactly like a sole proprietor—your LLC essentially doesn't exist for tax purposes. This is called "disregarded entity" status. You'll dump your business income and expenses onto Schedule C, calculate your profit, then pay that 15.3% self-employment tax on everything you earned. Let's say your LLC clears $80,000 after expenses. You're looking at roughly $12,240 in self-employment tax, plus your regular income tax on top of that.

Multiple owners change the default to partnership taxation. Your LLC files Form 1065, and each member gets a Schedule K-1 showing their slice of the pie. Active partners—meaning anyone involved in running the business—pay self-employment tax on their share of profits. The IRS occasionally recognizes "limited partners" who might escape self-employment tax on their distributions, but this rarely works for small businesses where everyone's involved in decisions.

Do distributions trigger self-employment tax? This question trips up nearly every new LLC owner. The answer: you're not taxed on distributions themselves. You're taxed on your share of the LLC's earnings, period. Whether you withdraw that money or leave it in the business account doesn't matter one bit.

Say you own half of an LLC that earned $200,000 profit this year. Your share is $100,000. You'll owe self-employment tax on that $100,000 even if the LLC only sent you $30,000 and kept the rest as working capital. The tax follows the earnings, not the distributions. This catches people off guard who think they're only taxed on money they actually receive.

Author: Olivia Carrington;

Source: worldwidemediums.net

How Different LLC Tax Elections Affect Self-Employment Tax

Your LLC doesn't have to accept its default tax treatment. You can file forms with the IRS to elect different tax classifications—and these elections completely reshape your self-employment tax situation.

Single-Member LLC Self-Employment Tax Treatment

Running a solo LLC in its default state gives you zero tax advantages over operating without any business entity. You're filling out Schedule C, calculating your net income, then multiplying by 15.3% for self-employment tax. Simple? Absolutely. Tax-efficient? Not remotely.

Take a marketing consultant whose one-person LLC nets $150,000 this year. She's paying approximately $22,950 just in self-employment tax. That's before she calculates her income tax liability. The $150,000 hits the Social Security ceiling (which is $168,600 in 2026), and Medicare tax applies to every dollar. She'll also owe federal income tax on the $150,000, though she gets to deduct half her self-employment tax when figuring her adjusted gross income.

The only escape from this scenario? File paperwork to change how the IRS taxes your LLC. The entity structure provides liability protection, but it won't reduce your tax bill without additional action.

Multi-Member LLC and Partnership Taxation

Adding partners increases complexity without automatically reducing self-employment tax. Each active member pays that 15.3% on their portion of business income.

Partnerships distinguish between guaranteed payments and distributive shares. Guaranteed payments—fixed compensation regardless of whether the business turns a profit—always carry self-employment tax. Your distributive share (your percentage of partnership profits) also triggers self-employment tax if you're a general partner participating in the business.

Some partnerships try getting creative by designating certain members as "limited partners" to dodge self-employment tax. The IRS scrutinizes these arrangements intensely. If you're making business decisions, providing substantial work, or presenting yourself as having authority, they'll classify you as a general partner. Your operating agreement might say "limited partner," but that won't convince an auditor if your actions say otherwise.

Author: Olivia Carrington;

Source: worldwidemediums.net

S Corporation Election and SE Tax Savings

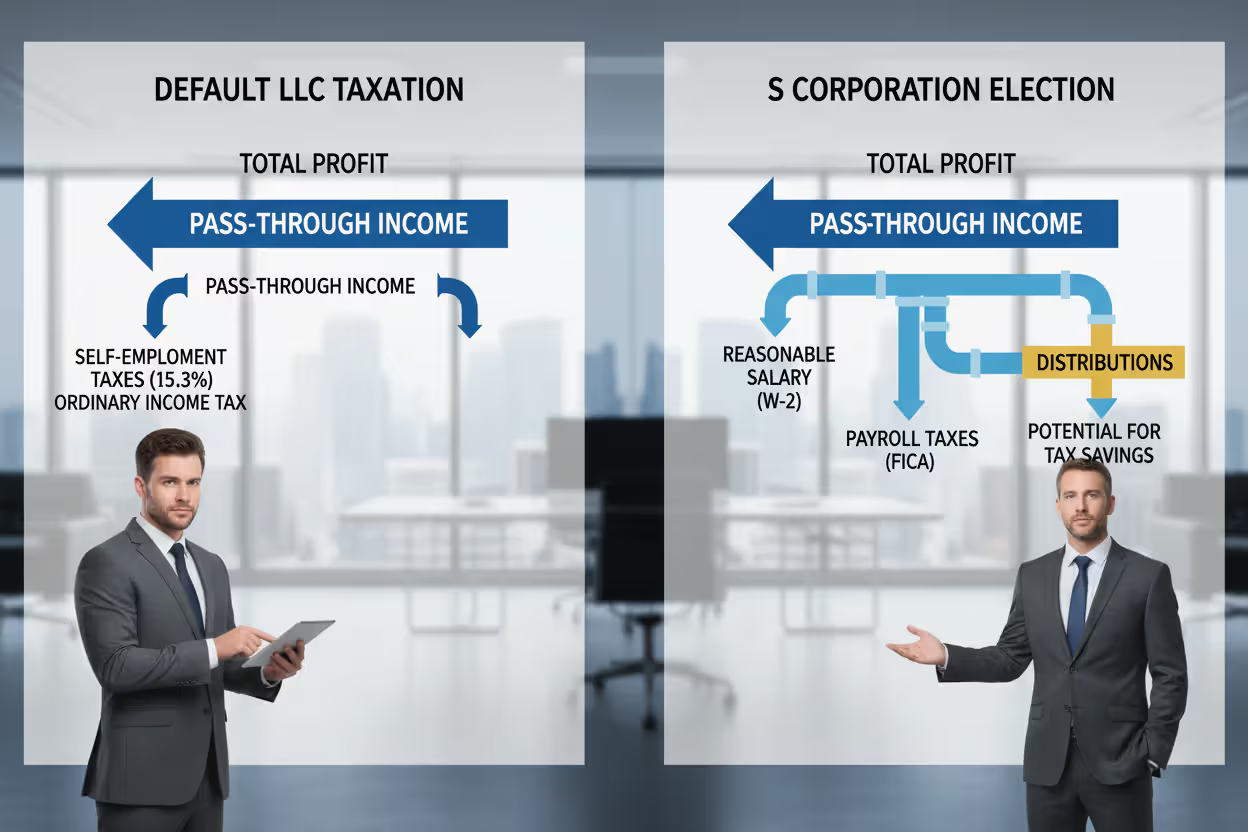

S corp election flips your entire tax strategy. Now you're required to split your money into two categories: wages for your work and distributions of profits. Only your wages face payroll taxes (the S corp equivalent of self-employment tax). Distributions escape that 15.3% entirely.

Here's the process: file Form 2553 electing S corporation treatment. Once approved, you become your own employee. You must establish payroll, pay yourself reasonable compensation for your services, withhold payroll taxes, and file quarterly employment tax returns. After you've paid yourself that reasonable salary, leftover profits can be distributed to you tax-free (beyond the income tax you already paid at the personal level).

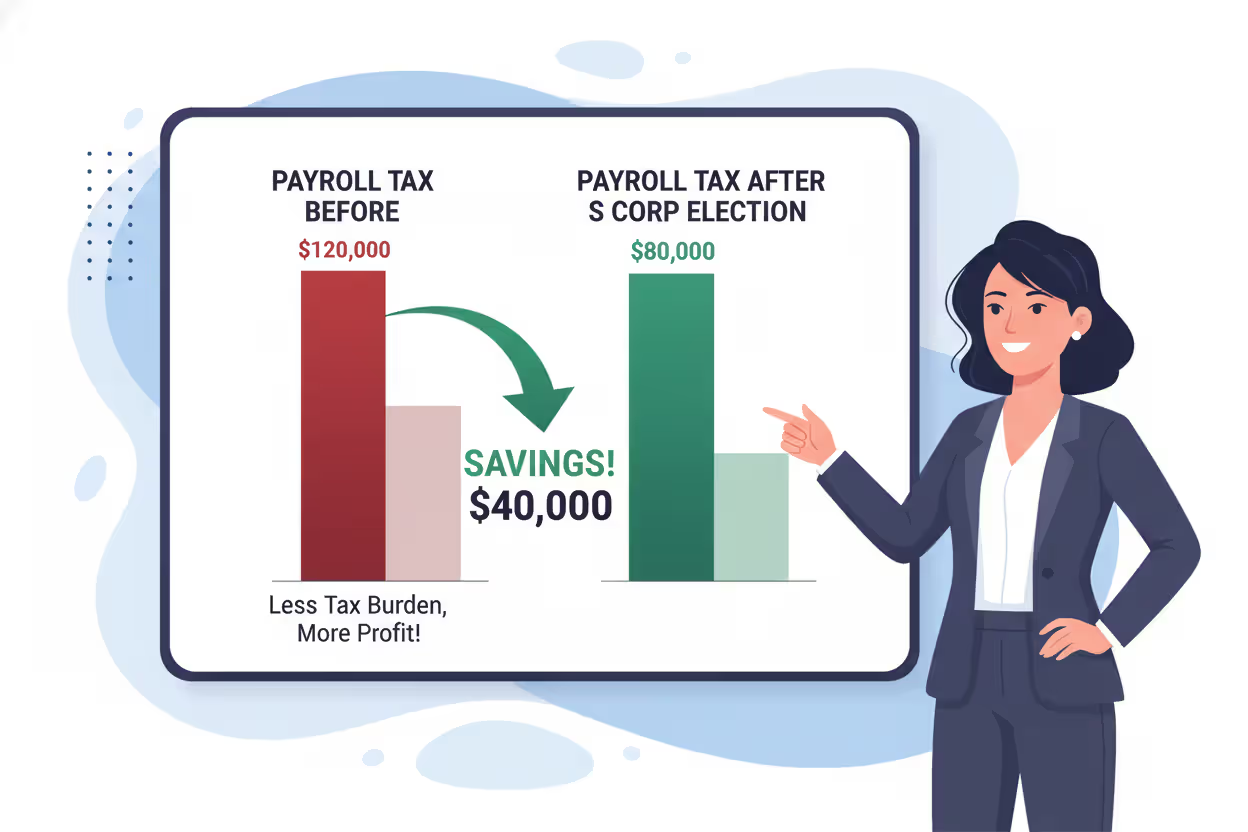

Back to our consultant earning $150,000. As an S corp, she might pay herself $90,000 in wages (reasonable for her experience and market rates) and take $60,000 as distributions. Payroll taxes apply only to the $90,000 salary—nothing additional on the $60,000 distribution. Her payroll tax drops from $22,950 down to approximately $13,770. She just saved $9,180.

The catch nobody wants to hear: "reasonable compensation" isn't optional. The IRS has decades of case law defining this. You must pay yourself what comparable businesses pay for comparable work in your industry and location. Try paying yourself $30,000 while taking $120,000 in distributions, and an audit is coming. When auditors find unreasonably low salaries, they'll reclassify your distributions as compensation, calculate what you should have paid in payroll taxes, then hit you with substantial penalties plus interest charges.

C Corporation Election

LLCs can elect C corp status, though it rarely makes sense when your goal is reducing self-employment tax. With C corporations, profits get taxed twice: first at the corporate level, then again when you receive dividends on your personal return. Owners who work in the business receive salaries subject to payroll taxes, just like S corps.

C corp status occasionally benefits businesses retaining significant earnings for expansion, seeking certain fringe benefit deductions, or preparing to raise venture capital. For self-employment tax reduction alone? S corp election beats C corp status in virtually every scenario.

Author: Olivia Carrington;

Source: worldwidemediums.net

How to Reduce Self-Employment Tax with an LLC

Everyone searches for "how to avoid self-employment tax with an LLC," but that phrasing sets up false expectations. You cannot legally eliminate self-employment tax while earning active business income. But you can definitely implement strategies to minimize what you pay.

S corporation election remains your most powerful weapon against self-employment tax. This strategy typically works best once your net income passes $60,000 to $80,000 annually. Below that threshold, you're spending more on payroll processing fees, extra tax return preparation, and state compliance costs than you're saving in taxes.

Run the numbers before making any election. Start with your current net business income. Subtract what represents reasonable compensation for someone doing your job (check industry salary surveys, talk to recruiters, review Bureau of Labor Statistics data). Multiply what's left by 15.3%—that's your potential annual savings. Business netting $120,000 with reasonable salary at $75,000? You'd save roughly $6,885 each year (15.3% of that $45,000 difference). The savings continue every year you maintain S corp status.

Every legitimate business expense you can document reduces your taxable profit before calculating self-employment tax. That means each dollar of valid deductions saves you approximately 15 cents in self-employment tax, plus whatever your income tax rate adds. Business owners frequently miss deductions for home office space, vehicle expenses, continuing education, software subscriptions, professional memberships, and business travel. Finding an additional $5,000 in legitimate deductions cuts your self-employment tax by roughly $765, plus income tax savings.

Retirement contributions offer another avenue, though they impact income tax more than self-employment tax. Self-employed people can fund SEP-IRAs or Solo 401(k) plans with substantial contributions. For 2026, Solo 401(k)s accept up to $23,500 in employee deferrals (higher if you're over 50) plus employer profit-sharing up to 25% of your compensation. These contributions reduce taxable income but don't reduce the self-employment tax you've already paid on business profit.

When you're self-employed and paying for health insurance, those premiums create an adjustment to income on your personal tax return. While this doesn't directly touch self-employment tax, it lowers your adjusted gross income and overall tax burden. S corporation owners can set up health reimbursement arrangements or factor health insurance into their W-2 compensation package.

Critical warning: any advertisement promising to "eliminate" or "completely avoid" self-employment tax is either promoting illegal tax evasion or misleading you about what's actually achievable. The IRS has encountered every scheme imaginable. Legitimate strategies involve proper elections, valid deductions, and careful planning—not tricks or loopholes.

Author: Olivia Carrington;

Source: worldwidemediums.net

Comparing LLC Tax Structures for Self-Employment Tax

Different tax elections create dramatically different obligations and requirements. Understanding the tradeoffs helps you select the right approach for your circumstances.

| Tax Structure | How SE Tax Is Applied | Tax Responsibility | Filing Requirements | Benefits | Drawbacks |

| Single-Member LLC (Default) | Full 15.3% applies to entire net profit | Owner reports everything on Schedule C | Schedule C, Schedule SE | Minimal paperwork; straightforward recordkeeping | Maximum SE tax; zero optimization opportunities |

| Multi-Member LLC (Default) | Each member pays 15.3% on their allocated share | Individual members report K-1 income | Form 1065, Schedule K-1, Schedule SE | Flexible profit splits; pass-through benefits | Active members all pay SE tax; partnership rules increase complexity |

| LLC as S Corp | Payroll tax only on salary portion; profit distributions avoid SE tax | Owner receives W-2 for salary; reports distributions separately | Form 1120-S, W-2, quarterly payroll filings | Substantial SE tax reduction; LLC liability protection maintained | Must defend reasonable salary; payroll compliance required; increased complexity |

| LLC as C Corp | Corporate earnings face entity-level taxation; payroll tax on wages | Corporation pays entity-level tax; owner pays on W-2 and dividends | Form 1120, W-2 | Certain fringe benefits; flexibility with retained earnings | Two layers of taxation; highest complexity; rarely best for SE tax purposes |

This breakdown shows why tax professionals typically recommend S corp election for profitable service businesses and consultants. The self-employment tax savings usually justify the extra administrative hassle once net income reaches that $60,000 to $80,000 range.

Your right answer depends on your specific numbers. Business clearing $40,000 profit? Single-member LLC simplicity probably wins. Business netting $200,000? You could save $15,000+ annually with S corp status, making the additional complexity and costs worthwhile.

Common Mistakes LLC Owners Make with Self-Employment Tax

Misunderstanding self-employment tax creates expensive problems. These mistakes show up constantly in small business tax situations.

Skipping quarterly estimated tax payments causes the most pain. Employees have taxes withheld automatically from every paycheck. LLC owners must calculate and remit estimated taxes every quarter. Miss these payments, and you'll owe underpayment penalties even when you pay your full tax bill by the April deadline. Tax law requires prepayment of at least 90% of your current year's tax liability or 100% of your previous year's total (increasing to 110% if last year's AGI topped $150,000). You cover this through withholding, estimated payments, or a combination of both.

Calculate quarterly payments by projecting your annual net profit, computing both self-employment and income tax on that projection, then dividing by four. Adjust your estimates mid-year if business income fluctuates significantly from your projection.

Mishandling distributions versus salary in S corporations creates serious IRS problems. Some S corp owners pay themselves tiny salaries—or nothing at all—while taking large distributions. The IRS has challenged and won these cases for decades. Courts consistently rule that working owners must receive reasonable compensation before distributions.

What counts as reasonable? Research what similar businesses pay for similar work in your geographic market. Industry associations publish salary data. Bureau of Labor Statistics provides benchmarks. Salary surveys from recruiting firms offer guidance. A real estate agent working 40 hours weekly in their S corp can't justify a $20,000 salary when comparable agents earn $75,000. When auditors discover unreasonably low compensation, they'll redesignate those distributions as wages, bill you for unpaid payroll taxes, and add significant penalties plus interest that compounds over time.

Not electing S corporation status when it makes financial sense leaves money on the table year after year. Many profitable LLC owners continue with Schedule C or partnership returns because they simply don't know S corp election could save thousands annually. The election requires filing Form 2553, typically by March 15 of the effective year (or within two months and 15 days of forming your LLC for first-year elections).

Sloppy recordkeeping undermines legitimate tax positions. When the IRS questions your reasonable salary determination, your expense deductions, or your income calculations, you need documentation to back up your positions. Bank statements, receipts, mileage logs, and contemporaneous records prove your case. Trying to reconstruct records years later during an audit rarely convinces auditors you're telling the truth.

Going it alone when situations get complex costs more than professional fees would have. DIY tax prep works fine for simple scenarios, but as income grows or you're considering S corp election, professional guidance pays for itself many times over. A qualified CPA can model different scenarios, ensure compliance, and spot opportunities you'd never find on your own.

When to Consult a Tax Professional About Your LLC

Certain situations demand professional advice rather than Google searches and guesswork.

Income thresholds matter enormously. Once your single-member LLC income or your share of multi-member LLC profits exceeds $60,000 to $80,000, book a consultation with a CPA who specializes in small business taxation. They'll analyze whether S corporation election makes financial sense after accounting for payroll costs, additional preparation fees, and state-specific factors. That analysis might take an hour but could save you thousands every year going forward.

State rules complicate everything. Some states don't recognize S elections or impose extra taxes on S corps. California hits S corporations with an annual minimum franchise tax plus a gross receipts fee that scales with revenue. New York City's unincorporated business tax may apply differently depending on your structure. A tax professional familiar with your state's specific rules prevents expensive mistakes.

Complex multi-member arrangements require professional help. When LLC members contribute different capital amounts, provide different service levels, or want profit allocations that don't match ownership percentages, partnership tax rules get intricate fast. Special allocations must satisfy "substantial economic effect" requirements under IRS regulations. Guaranteed payments, preferred returns, and distribution waterfalls need proper structuring and documentation.

Major changes in your personal or business situation call for a tax structure review. Marriage, divorce, bringing on new partners, expanding to multiple states, hiring employees for the first time, or experiencing significant income swings all affect your optimal structure. An annual review with a tax professional ensures your LLC election still serves your best interests.

The biggest mistake I see is business owners waiting until they have a tax problem to seek advice.Proactive tax planning—choosing the right LLC structure before you need it, making elections on time, and implementing strategies throughout the year—saves far more money than trying to fix problems after the fact. Self-employment tax planning isn't about finding loopholes; it's about using the tax code's legitimate options to your advantage

— Jennifer Martinez

Frequently Asked Questions

Self-employment tax hits LLC owners hard, but understanding how different structures affect your obligation empowers you to make informed choices. The election you make for your LLC—not the entity formation itself—directly determines how much you'll send to the IRS each year in self-employment tax.

Default LLC structures prioritize simplicity over tax savings. Single-member LLCs and multi-member LLCs operating as partnerships require that full 15.3% self-employment tax on all net business income from active work. This straightforward treatment works well for new ventures, businesses with modest profits, or owners who value simplicity above tax optimization.

S corporation election delivers the most effective self-employment tax reduction once your income justifies the extra administrative work. Dividing compensation between reasonable salary and distributions saves thousands annually in payroll taxes. The strategy demands careful execution—especially regarding reasonable salary justification—but tax savings typically dwarf the complexity once businesses clear $60,000 net income.

Legitimate expense deductions, retirement contributions, and thorough recordkeeping complement whatever structural decisions you make. Every dollar of valid expenses reduces both taxable income and self-employment tax liability. Maintaining detailed records protects your tax positions and provides ammunition if the IRS ever questions your return.

The worst decision is making no decision. Too many LLC owners stick with default tax treatment year after year, completely unaware that filing simple paperwork could substantially cut their tax burden. Others make elections without understanding compliance requirements, creating audit problems down the road.

Review your LLC's tax structure every year, particularly as income grows or circumstances shift. What made perfect sense when you launched your business might be costing you thousands three years later. Spending a few hundred dollars consulting a qualified tax professional can save thousands in taxes and help you sidestep costly compliance mistakes.

Self-employment tax planning isn't about dodging obligations—it's about intelligently using the tax code's legitimate provisions to structure your business efficiently. The IRS provides multiple options for organizing and taxing your LLC. Understanding those options and choosing strategically keeps more money working in your business instead of disappearing into tax payments.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to Limited Liability Companies (LLCs), including formation, management, taxation, compliance, and business structuring.

All information on this website, including articles, guides, templates, and examples, is presented for general educational purposes. LLC requirements and regulations may vary depending on individual circumstances, business activities, state laws, and jurisdiction.

This website does not provide legal, tax, or financial advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.